A Message From Cboe Europe President David Howson

David Howson

▬

April 23, 2020

David Howson, President, Cboe Europe, reached out to European customers at the end of April with an update on the current market environment. Read his letter below.

Dear Cboe Europe Participants and Members of the Trading Community,

I hope you’re all safe and well in these unprecedented times.

I’m aware this is the first time I’ve communicated with you all in my new role, but it is something I will endeavour to do on a regular basis. While I would have liked this first update to have been in less challenging circumstances for all of us, I’m honoured to work with all of you during these extraordinary times and into the future to continue to execute Cboe Europe’s longstanding strategy of bringing competition and innovation to European markets.

With the first quarter behind us, I thought it would be timely to provide a brief update on some key initiatives, the European equity market’s response to the COVID-19 crisis and some of our thoughts on ESMA’s consultation on the equity aspects of the MiFID II/MiFIR review.

Market Updates

Our pending acquisition of pan-European clearing house EuroCCP is progressing well, pending the receipt of required regulatory clearances and the arrangement of a supporting liquidity facility at the EuroCCP clearing entity level. This acquisition is expected to pave the way for the launch of Cboe Europe Derivatives, a new pan-European derivatives market. We’ll be announcing additional details on this initiative soon, so stay tuned.

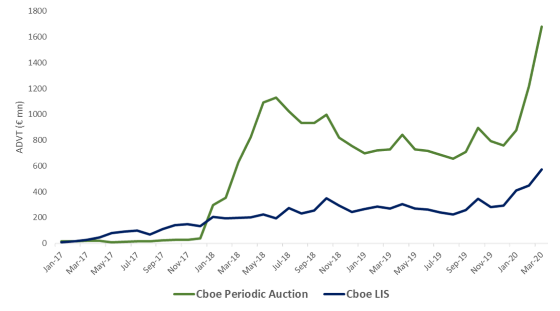

Turning now to recent market conditions. Like many operators, we experienced all-time record volumes across many of our platforms in March, including Periodic Auctions and Cboe LIS, and we should all take comfort from the fact that Europe’s market infrastructure stood up extremely well to the high levels of activity. That is testament to the work of all participants: Markets have been functioning as they should, investors have been able to manage risk appropriately and it was absolutely the right call for markets to stay open.

It is all the more incredible given the work-from-home policies we’re all now operating under – for Cboe Europe’s part, we moved all staff to remote working in London and Amsterdam in early March, without any operational issues or loss of focus on projects to improve markets for participants. What this period has demonstrated is the strength and resilience of European market structure and the eco-system that exists. It is something we need to preserve – and enhance, where appropriate.

ESMA MiFID II/MiFIR Consultation

On that note, last week we submitted our response to ESMA on its MiFID II/ MiFIR review report on the transparency regime for equity and equity-like instruments, and I want to express my thanks to those who provided feedback to help inform our response. We believe, as I’m sure most market participants do, that many of the areas consulted on need careful consideration in order to avoid causing damage to European equity market structure and we have provided a robust response, which is available here.

Given the significance of this consultation I wanted to share some of the key points we outlined in our response to ESMA:

- A healthy eco-system of complementary execution mechanisms is necessary to support a diverse range of trading strategies and different market conditions. This has developed since MiFID I allowed competition, to the benefit of end investors, and having this choice is particularly important in low volume environments as well as during extreme market stress, as we saw during March.

- We believe there is no fundamental issue with the balance of trading between available mechanisms and there is an ongoing predominance of lit markets, particularly central limit order books. This becomes apparent when activity that is technical in nature and therefore not appropriate for execution on a multilateral venue is removed from the picture. The ESMA consultation is unhelpful in the way that it presents non pre-trade transparent trading as including all SI and OTC activity, as well as all activity undertaken under a waiver.

- With that in mind, retaining choice for investors is key – this includes all waivers and the SI category. Reference price waiver systems in particular are highly valued by investors to satisfy their demand for urgent, low-impact midpoint executions. There needs to be a commitment from regulators to ensuring any proposed enhancements/changes are justified in terms of better outcomes for the end users of markets – investors and issuers.

- While we recognise the effort and associated cost of implementing the double volume cap (DVC) regime, we believe the caps should be removed in their entirety rather than arbitrary alterations made to the current thresholds. The DVCs have introduced cost and complexity and delivered no clear benefit to execution performance and end investors.

- While we understand the MiFID II review represents an opportunity to enshrine in legislation the conclusions ESMA previously reached with respect to periodic auctions, we believe no evidence of investor detriment exists to justify materially different regulatory intervention at this time. The platforms, including the enhancements ESMA proposed last year, have proven themselves as low impact, price-forming mechanisms that deliver beneficial execution outcomes.

- Finally, we believe the significant increase in closing auction volume poses a systemic risk to the efficient and orderly running of markets and should be closely monitored by regulators. This trend would be further exacerbated if the choice of low impact trading mechanisms, such as those utilising the RPW and NTW, is forcefully reduced.

I’d be happy to discuss any aspect of our response with you and welcome any feedback on our recommendations.

I look forward to the next time we can gather again as an industry and until then, stay healthy and safe.

Regards,

David Howson

President

Cboe Europe

Related Posts