Inside Volatility Trading: More Chaos Ahead – Or a Bottom? What Does the VIX Index Say?

Scott Bauer

▬

May 23, 2022

The VIX® Index – which measures the expectation of stock-market volatility as expressed by options prices – stands far above its long-term median level of 17.6. Yet, as discussed in a recent Reuters article, what some investors might view as lack of panic in the U.S. stock market, at least as measured by Wall Street’s "fear gauge," may be keeping those investors from putting cash to work after a massive selloff. The VIX Index can spike when investor concerns are heightened by events like the Covid-19 pandemic, the angst of the Fed raising rates, or the ongoing geo-political risk between Russia and Ukraine. Investors and traders alike have been on a roller-coaster ride, but some investors may believe that the VIX Index has yet to convincingly signal that the sell-off has reached its end.

Since 1990, after major market declines, the Cboe Volatility Index® (the VIX® Index) has averaged a reading of 37 compared to its most recent level of approximately 30. Though the VIX Index has hit this level multiple times since late February, most recently at the beginning of May, it has yet to break through and hit that level of “capitulation” that some investors may be waiting for. Some investors may believe that means the true “I give up” scenario that sometimes accompanies past market bottoms has yet to be seen, despite the S&P 500 Index having fallen almost 20% from its all time high. This is a level that would put the index into bear market territory. While it is not necessary for the VIX Index to shoot higher before calm returns to markets, the current landscape may make it more difficult to buy on further weakness.

In March 2020, during the COVID-19 selloff, the VIX peaked out at its all-time high close of 82.69. The S&P 500 index subsequently more than doubled as interest rates were slashed and other easy money policies helped support the economy. The VIX Index topped out at 80.86 during the Great Recession and hit 36.07 in 2018, when stocks stopped just short of entering a bear market on worries over tighter Federal Reserve monetary policy.

Sector 500-Trading Day Forward Returns by Rolling 14-Day VIX

(1998 – Current)

You can see that the opportunities when the VIX Index is above the mid-30’s are uncommon, but we have been in that general area for the last month. Just because the VIX Index moves above that level doesn’t mean it can’t go higher and it’s not necessarily an indication of a bottom either, but historically this can offer the possibility to capture above average gains moving forward as reflected by the chart above.

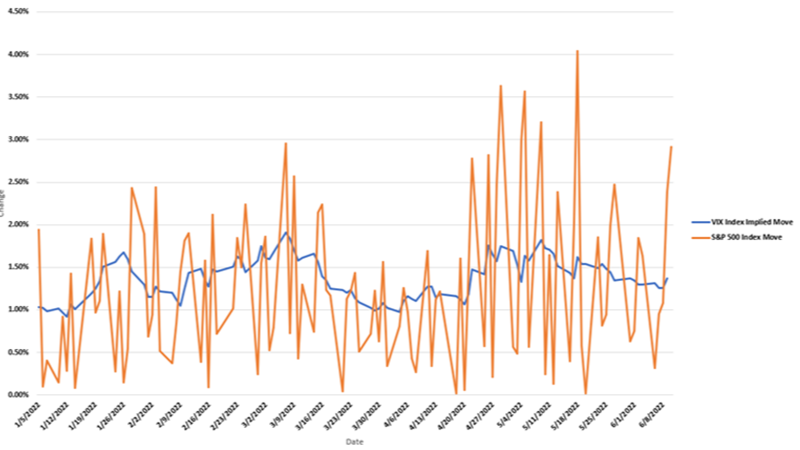

The VIX Index uses calendar day annualization so a VIX Index at 28 represents a daily move in the S&P 500 Index of approximately 1.47% (28/SQRT of 365), or 59 points. However, the S&P 500 Index has moved more than that in a majority of the sessions over the last few weeks.

The VIX Index is calculated based on at-the-money S&P 500 index option contracts. Reuters notes that one reason the VIX may not be breaking out signaling a possible capitulation is that the current selloff, though steep, has been a gradual one. This may have allowed investors to exit positions along the way. According to analysts at Deutsche Bank, investors' aggregate equity positioning has slipped to the lowest levels since the 2020 COVID-19 selloff.

VIX Index Closing Value

The markets are still trying to digest rising interest rates, seemingly unstoppable inflation and the continued war in Ukraine. This has frayed consumer confidence and has led investors to believe that volatility is likely to remain elevated for several months, if not longer. The S&P 500 Index has dropped below major technical support areas while the NASDAQ-100 Index remains solidly in bear-market territory and has fallen to a new 18-month low.

Industry News

- Reuters: Bitcoin set for record losing streak after ‘stablecoin’ collapse

- Wall Street Journal: Crash of TerraUSD Shakes Crypto. ‘There Was a Run on the Bank.’

- Tech Crunch: Binance halts Luna and UST trading across spot pairs

- Yahoo Finance: Robinhood shares surge after Sam Bankman-Fried discloses stake

- Bloomberg: Is a Blacklash Brewing Against ‘Woke’ ETF Giants?

- Markets Media: Options-Market Cyberhacks on the Rise

- Markets Media: ICE Raises $8bn for Black Knight Acquisition

- Yahoo Finance: LME Seeks Increased Transparency to Prevent Repeat of Nickel Squeeze

Events

- May 25-26: Global EQD

- May 25: New Research Papers for Investors and Traders

- June 8: Russell Reconstitution & Income Generating Opportunities

- June 16: Volume, Liquidity & Performance

Volatility411

Get This Newsletter Sent to Your Inbox

Get the Inside Volatility Trading newsletter directly in your inbox by signing up here.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers below.

General

The information provided is for general education and information purposes only. No statement provided should be construed as a recommendation to buy or sell a security, future, financial instrument, investment fund, or other investment product (collectively, a “financial product”), or to provide investment advice.

In particular, the inclusion of a security or other instrument within an index is not a recommendation to buy, sell, or hold that security or any other instrument, nor should it be considered investment advice.

Options

Options involve risk and are not suitable for all market participants. Prior to buying or selling an option, a person should review the Characteristics and Risks of Standardized Options (ODD) , which is required to be provided to all such persons. Copies of the ODD are available from your broker or from The Options Clearing Corporation, 125 S. Franklin Street, Suite 1200, Chicago, IL 60606.

Trading FLEX options may not be suitable for all options-qualified market participants. FLEX options strategies only should be considered by those with extensive prior options trading experience.

Uncovered option writing is suitable only for the knowledgeable market participant who understands the risks, has the financial capacity and willingness to incur potentially substantial losses, and has sufficient liquid assets to meet applicable margin requirements. In this regard, if the value of the underlying instrument moves against an uncovered writer's options position, the writer may incur large losses in that options position and the participant’s broker may require significant additional margin payments. If a market participant does not make those margin payments, the broker may liquidate positions in the market participant’s account with little or no prior notice in accordance with the market participant’s margin agreement.

Futures

Futures trading is not suitable for all market participants and involves the risk of loss, which can be substantial and can exceed the amount of money deposited for a futures position. You should, therefore, carefully consider whether futures trading is suitable for you in light of your circumstances and financial resources. You should put at risk only funds that you can afford to lose without affecting your lifestyle.

For additional information regarding the risks associated with trading futures and security futures, see respectively the Risk Disclosure Statement set forth in Appendix A to CFTC Regulation 1.55(c) and the Risk Disclosure Statement for Security Futures Contracts.

VIX® Index and VIX® Index Products

The Cboe Volatility Index® (known as the VIX Index) is calculated and administered by Cboe Global Indices, LLC. The VIX Index is a financial benchmark designed to be a market estimate of expected volatility of the S&P 500® Index, and is calculated using the midpoint of quotes of certain S&P 500 Index options as further described in the methodology, rules and other information here .

VIX futures and Mini VIX futures, traded on Cboe Futures Exchange, LLC, and VIX options, traded on Cboe Options Exchange, Inc. (collectively, “VIX® Index Products”), are based on the VIX Index. VIX Index Products are complicated financial products only suitable for sophisticated market participants.

Transacting in VIX Index Products involves the risk of loss, which can be substantial and can exceed the amount of money deposited for a VIX Index Product position (except when buying options on VIX Index Products, in which case the potential loss is limited to the purchase price of the options).

Market participants should put at risk only funds that they can afford to lose without affecting their lifestyles.

Before transacting in VIX Index Products, market participants should fully inform themselves about the VIX Index and the characteristics and risks of VIX Index Products, including those described here. Market participants also should make sure they understand the product specifications for VIX Index Products ( VIX futures , Mini VIX futures and VIX options ) and the methodologies for calculating the underlying VIX Index and the settlement values for VIX Index Products. Answers to questions frequently asked about VIX Index products and how they are settled is available here .

Not Buy and Hold Investment: VIX Index Products are not suitable to buy and hold because:

- On their settlement date, VIX Index Products convert into a right to receive or an obligation to pay cash.

- The VIX Index generally tends to revert to or near its long-term average, rather than increase or decrease over the long term.

Volatility: The VIX Index is subject to greater percentage swings in a short period of time than is typical for stocks or stock indices, including the S&P 500 Index.

Expected Relationships: Expected relationships with other financial indicators or financial products may not hold. In particular:

- Although the VIX Index generally tends to be negatively correlated with the S&P 500 Index – such that one tends to move upward when the other moves downward and vice versa – that relationship is not always maintained.

- The prices for the nearest expiration of a VIX Index Product generally tend to move in relationship with movements in the VIX Index. However, this relationship may be undercut, depending on, for example, the amount of time to expiration for the VIX Index Product and on supply and demand in the market for that product.

- Mini VIX futures contracts trade separately from regular-sized VIX futures, so the prices and quotations for Mini VIX futures and regular-sized VIX futures may differ because of, for example, possible differences in the liquidity of those markets.

Final settlement Value: The method for calculating the final settlement value of a VIX Index Product is different from the method for calculating the VIX Index at times other than settlement, so there can be a divergence between the final settlement value of a VIX Index Product and the VIX Index value immediately before or after settlement. (See the SOQ Auction Information section here for additional information.)

Exchange Traded Products ("ETPs")

Cboe does not endorse or sell any ETP or other financial product, including those investment products that are or may be based on a Cboe index or methodology or on a non-Cboe index that is based on investment products trading on a Cboe Company exchange (e.g., VIX futures); and Cboe makes no representations regarding the advisability of investing in such products. An investor should consider the investment objectives, risks, charges, and expenses of these products carefully before investing. Investors also should carefully review the information provided in the prospectuses for these products.

Investments in ETPs involve risk, including the possible loss of principal, and are not appropriate for all investors. Non-traditional ETPs, including leveraged and inverse ETPs, pose additional risks and can result in magnified gains or losses in an investment. Specific risks relating to investment in an ETP are outlined in the fund prospectus and may include concentration risk, correlation risk, counterparty risk, credit risk, market risk, interest rate risk, volatility risk, tracking error risk, among others. Investors should consult with their tax advisors to determine how the profit and loss on any particular investment strategy will be taxed.

Cboe Strategy Benchmark Indices

Cboe Strategy Benchmark Indices are calculated and administered by Cboe Global Indices, LLC as described in the methodologies, rules and other information available here using information believed to be reliable, including market data from exchanges owned and operated by other Cboe Companies.

Strategy Benchmark Indices are designed to measure the performance of hypothetical portfolios comprised of one or more derivative instruments and other assets used as collateral. Past performance is not indicative of future results. Strategy Benchmark Indices are not financial products that can be invested in directly, but can be used as the basis for financial products or managing portfolios.

The actual performance of financial products such as mutual funds or managed accounts can differ significantly from the performance of the underlying index due to execution timing, market disruptions, lack of liquidity, brokerage expenses, transaction costs, tax consequences and other considerations that may not be applicable to the subject index. Index and Benchmark Values Prior to Launch Date

Index and benchmark values for the period prior to an index’s launch date are calculated by a theoretical approach involving back-testing historical data in accordance with the methodology in place on the launch date (unless otherwise stated). A limitation of back-testing is that it reflects the theoretical application of the index or benchmark methodology and selection of the index’s constituents in hindsight. Back-testing may not result in performance commensurate with prospective application of a methodology, especially during periods of high economic stress in which adjustments might be made. No back-tested approach can completely account for the impact of decisions that might have been made if calculations were made at the same time as the underlying market conditions occurred. There are numerous factors related to markets that cannot be, and have not been, accounted for in the preparation of back-tested index and benchmark information.

Taxes

No Cboe Company is an investment adviser or tax advisor, and no representation is made regarding the advisability or tax consequences of investing in, holding or selling any financial product. A decision to invest in, hold or sell any financial product should not be made in reliance on any of the statements or information provided. Market participants are advised to make an investment in, hold or sell any financial product only after carefully considering the associated risks and tax consequences, including information detailed in any offering memorandum or similar document prepared by or on behalf of the issuer of the financial product, with the advice of a qualified professional investment adviser and tax advisor.

Under section 1256 of the Tax Code, profit and loss on transactions in certain exchange-traded options and futures are entitled to be taxed at a rate equal to 60% long-term and 40% short-term capital gain or loss, provided that the market participants involved and the strategy employed satisfy the criteria of the Tax Code. Market participants should consult with their tax advisors to determine how the profit and loss on any particular option or futures strategy will be taxed. Tax laws and regulations change from time to time and may be subject to varying interpretations.

General

Past performance of an index or financial product is not indicative of future results.

Brokerage firms may require customers to post higher margins than any minimum margins specified.

No data, values or other content contained in this document (including without limitation, index values or information, ratings, credit-related analyses and data, research, valuations, strategies, methodologies and models) or any part thereof may be modified, reverse-engineered, reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of Cboe.

Cboe does not guarantee the accuracy, completeness, or timeliness of the information provided. THE CONTENT IS PROVIDED “AS IS” WITHOUT WARRANTY OF ANY KIND, EITHER EXPRESS OR IMPLIED, INCLUDING, WITHOUT LIMITATION, ANY WARRANTY WITH RESPECT MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE.

Hypothetical scenarios are provided for illustrative purposes only. The actual performance of financial products can differ significantly from the performance of a hypothetical scenario due to execution timing, market disruptions, lack of liquidity, brokerage expenses, transaction costs, tax consequences and other considerations that may not be applicable to the hypothetical scenario.

Supporting documentation for statements, comparisons, statistics or other technical data provided is available by contacting Cboe at www.cboe.com/Contact .

The views of any third-party speakers or third-party materials are their own and do not necessarily represent the views of any Cboe Company. That content should not be construed as an endorsement or an indication by Cboe of the value of any non-Cboe financial product or service described.

The inclusion of research not conducted or explicitly endorsed by Cboe should not be construed as an endorsement or indication of the value of that research.

Trademarks and Intellectual Property

Cboe®, Cboe Global Markets®, Bats®, BIDS Trading®, BYX®, BZX®, Cboe Options Institute®, Cboe Vest®, Cboe Volatility Index®, CFE®, EDGA®, EDGX®, Hybrid®, LiveVol®, Silexx® and VIX® are registered trademarks, and Cboe Futures ExchangeSM, C2SM, f(t)optionsSM, HanweckSM, and Trade AlertSM are service marks of Cboe Global Markets, Inc. and its subsidiaries. Standard & Poor's®, S&P®, S&P 100®, S&P 500® and SPX® are registered trademarks of Standard & Poor's Financial Services LLC and have been licensed for use by Cboe Exchange, Inc. Dow Jones®, Dow Jones Industrial Average®, DJIA® and Dow Jones Global Indexes® are registered trademarks or service marks of Dow Jones Trademark Holdings, LLC, used under license. Russell, Russell 1000®, Russell 2000®, Russell 3000® and Russell MidCap® names are registered trademarks of Frank Russell Company, used under license. FTSE® and the FTSE indices are trademarks and service marks of FTSE International Limited, used under license. MSCI and the MSCI index names are service marks of MSCI Inc. (“MSCI”) or its affiliates and have been licensed for use by Cboe. All other trademarks and service marks are the property of their respective owners.

Copyright

© 2022 Cboe Exchange, Inc. All Rights Reserved.

Related Posts