Global Markets

Tradable Products

Featured Products

By Matthew Healey, North American Equities Execution Consulting

In 2013, odd lots, or orders less than 100 shares, started printing to the tape. Since then, odd lots have become a significant component of the market, with recent growth caused by the proliferation of commission free trades and the introduction of novel retail trading platforms.

One of the recommendations in Cboe’s Market Policy and Government Affairs (MPGA) team’s recently published Vision for Targeted Equity Market Structure Improvements was to remove the exemption for not displaying customer odd lot orders to further encourage limit order placement in the public markets.

In the study below, Cboe’s Equities Execution Consulting team examines the amount of odd lot liquidity available in the market, when odd lot orders are most active, how these orders impact the National Best Bid and Offer (NBBO), and their composition in symbols based on price and liquidity.

Odd lots currently represent 54.8% of all trades in the U.S. financial markets, up from 43% at the beginning of 2020. During the initial pandemic-related volatility in March 2020, odd lot executed share volume spiked to almost one billion shares per day, as illustrated in the chart below. Odd lot executed share volume reached its peak during the ‘meme’ stock phenomenon observed in early 2021. While odd lot average daily executed share volume has decreased about 22% from the highs reached in February and March, their percentage of trades continues to increase, and overall share volume remains higher than the prior year.

Figure 1 - Odd Lots ADV & Percentage of Trades

Data Source: SIP, Cboe

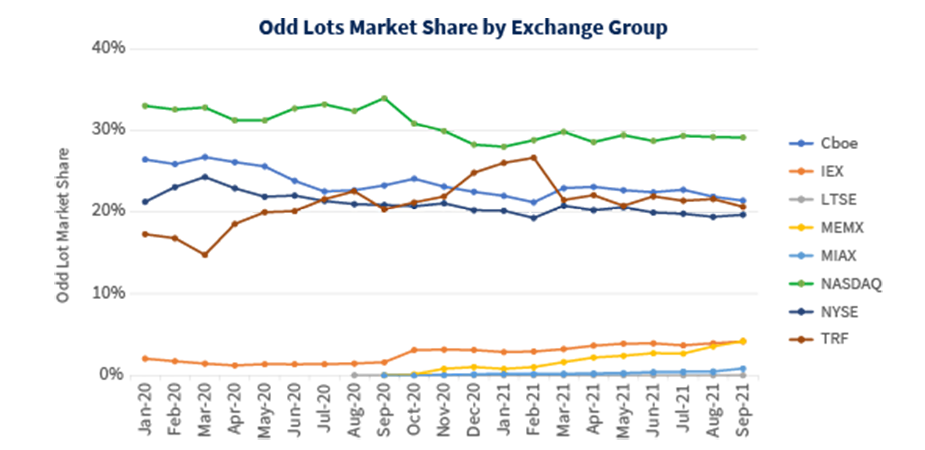

We believe Cboe’s innovative Retail Priority Program on EDGX® Equities Exchange helped drive Cboe’s combined markets to capture 21.4% of total odd lot share volume, second only behind Nasdaq. As of September 2021, the FINRA Trade Reporting Facility (TRF) accounts for 20.6% of odd lot share volume, an increase of about 3.4% since January 2020.

Figure 2 - Odd Lots TCV Market Share by Exchange Group

Data Source: SIP, Cboe

The increase in odd lot trading was not localized to the most actively traded stocks, but across all stocks. Stocks in the chart below are organized into quintiles by total executed share volume for 2021, which we then used to calculate the average percentage of share volume that traded in odd lots for all stocks in each quantile. As total volume increased, odd lots represented a smaller percentage of the overall share volume. On average, odd lots represented about 28% of share volume for stocks in the bottom 20th volume percentile. However, for the most liquid stocks this year — stocks in the greater than 80th volume percentile —odd lots accounted for about 10.7% of share volume.

Figure 3 - Odd Lots Percentage of Volume by Total Volume Percentile

Data Source: SIP, Cboe

Additionally, we analyzed odd lot share volumes relative to stock price. The chart shows the average percentage of share volume by stock price for odd lots since the beginning of 2020. As stock price increases, odd lot share volume percentage also increases. Since first-quarter 2020 the percentage of odd lots has increased across all price groups. The largest increase was in stocks priced between $100 and $499.99, where odd lots increased 3.3% to comprise 15.2% of share volume. For stocks priced greater than $500, the odd lot percentage has increased about 2.3% since first-quarter 2020, representing about 34% of share volume in these stocks in third-quarter 2021.

Figure 4 - Average Odd Lots Percentage of Volume by Share Price

Data Source: SIP, Cboe

We then analyzed stocks by share price, separating the total size of odd lot orders into five groups and computing the percentage of orders each price group represents. Stocks greater than $100 represented about 40% of single-share trades. As the size of the order increases, the percentage decreases, with the percentage of total trades for stocks priced greater than $100 decreasing to about 18%. Stocks priced between $5 and $49.99 represent about 35% of single-share trades. However, in trades where the size equals 100 shares, this price group represents about 53% of trades, highlighting that the price of a stock appears to have a significant impact on the size of the order submitted.

Figure 5 - Price Group Percentage of Orders by Order Size

Data Source: SIP, Cboe

To further highlight odd lot growth over the past few years, we analyzed odd lot share volume by time of day. The chart below illustrates average odd lot market share for every hour throughout the entire trading day, inclusive of pre- and post-markets. Overall, odd lot market share of share volume has steadily increased since 2019, with significant growth in the pre- and post-market sessions.

Figure 6 - Odd Lots TCV Market Share by Time (Hourly)

Data Source: SIP, Cboe

Similar to our previous analysis of the growth in retail trading sparked by social media, we examined the top 15 “meme” stocks mentioned daily on Reddit’s r/wallstreetbets discussion board and found the mentions are correlated to odd lot share volumes. The chart below shows the daily percentage of total odd lot share volume and the overall percentage of total composite volume (TCV) for the top 15 most discussed stocks. There appears to be a direct correlation between trading of the most popular meme stocks and odd lots. On days when meme stocks represent a large portion of overall TCV, the stocks also make up a significant amount of total odd lot share volume. We calculated the correlation to determine the strength of the relationship and found a coefficient of determination of 0.60, which represents a moderately strong correlation.

On January 27, during the peak of the GameStop trading phenomenon, total odd lot share volume for the top 15 meme stocks reached a high of 13%. Similarly, at the end of May, when the same retail stocks started to gain momentum again, the stocks represented over 10% of odd lot share volume on multiple days.

Figure 7 - Top 15 “Meme” Stocks Percentage of Odd Lots Volume

Data Source: SIP, Cboe

Cboe’s MPGA team also advocated for odd lots to be represented on the quote in its Vision for Targeted Equity Market Structure Improvements. We analyzed orders on Cboe’s four equities exchanges (EDGX, EDGA®, BZX® and BYX®) and where they rest relative to the NBBO at entry. Odd lots currently make up 20.6% of orders on Cboe exchanges, demonstrated below. In September 2021, odd lots represented about 6.3% of executed share volume across all four exchanges, an increase of about 2.2% since the beginning of the year.

Figure 8 - Odd Lots Percentage of Orders on Cboe Exchanges

Data Source: SIP, Cboe

The chart below illustrates where odd lot orders stand relative to the NBBO when entered (Away, At NBBO, Better than NBBO and Spread Crossing) by the stock’s total volume. Odd Lot orders that had a limit price better than the NBBO, represented about 59.6% of orders in the bottom 20th volume percentile. However, as total executed share volume increased, the number of orders better than the spread decreased. Odd lot orders that were priced away from the NBBO increased as total share volume increased. In the top 80th volume percentile, orders priced worse than the NBBO accounted for about 28.6% of orders compared to just 9.1% in less liquid stocks.

There is still a significant amount of odd lot orders that are at or better than the NBBO. In more liquid stocks, the number of odd lot orders priced at or better than the NBBO represents between 70-80% of all odd lot orders, similar to trends observed in 2020.

Figure 9 - Odd Lots Percentage of Volume by Total Volume Percentile

Data Source: SIP, Cboe

Finally, we analyzed odd lot orders on Cboe exchanges that had a limit price better than the NBBO. The breakdown by spread in cents demonstrates how much these orders can improve the NBBO grouped by stock’s total volume. In less liquid stocks, there is a significant number of orders with a spread greater than 50 cents at 28.2%. This number steadily decreases as total volume increases, while odd lot orders that had a tighter spread of 1 to 5 cents drastically increased as the executed volume percentile increased. Orders with a spread 1 to 5 cents wide represented about 8.5% in the less than 20th percentile, while the most liquid stocks in the 80th percentile made up almost 30% of the orders. This shows that odd lot orders can have a meaningful impact on improving the NBBO across the entire universe of stocks.

Figure 10 - Odd Lots Better than the NBBO Percentage of Orders by Spread

Data Source: SIP, Cboe

Once considered an afterthought, odd lots are an integral and valuable part of today’s vibrant markets. This growing segment is a meaningful source of liquidity across all trading periods and stocks. The significant price improvement that odd lots represent on Cboe’s exchanges, and likely on other similar exchanges as well, should be displayed to all market participants. In addition to adding odd lots to the displayed quote, updating the order size requirements of the Limit Order Display Rule would further improve the U.S. markets. Furthermore, changing Rule 604’s notional threshold from $100,000 to $500,000, along with the 10,000 share requirement, while also adding a minimum of $1,000 notional, would further enhance the quality of the displayed markets for all participants. Please reach out to Cboe’s North American equities coverage team with further questions and to learn how we can help you optimize your trading experience.

2021 Cboe Exchange, Inc. All rights reserved.

The information provided is for general education and information purposes only. No statement provided should be construed as a recommendation to buy or sell a security, future, financial instrument, investment fund, or other investment product (collectively, a “financial product”), or to provide investment advice

Cboe®, Cboe Global Markets®, Bats®, BIDS Trading®, BYX®, BZX®, Cboe Options Institute®, Cboe Vest®, Cboe Volatility Index®, CFE®, EDGA®, EDGX®, Hybrid®, LiveVol®, Silexx® and VIX® are registered trademarks, and Cboe Futures ExchangeSM, C2SM, f(t)optionsSM, HanweckSM, and Trade AlertSM are service marks of Cboe Global Markets, Inc. and its subsidiaries.

Past performance of an index or financial product is not indicative of future results. Click Here to Unsubscribe. To unsubscribe by postal mail, please write to: Cboe Customer Experiences, 400 S. LaSalle St., Chicago, IL 60605 © 2021 Cboe Exchange, Inc. All Rights Reserved.