Global Markets

Tradable Products

Featured Products

How many equity destinations can you trade on? This month, the industry has seen the launch of three new trading venues on top of the existing 13. While this number seems intimidating, increased competition may have some benefits for investors. Each market participant must allocate resources and determine how each market center benefits them. Those benefits depend on the type of flow each industry participant services. To further explore the current liquidity landscape, it is important to first understand each type of market center.

Current Liquidity Landscape

The current market centers for market participants may be classified by the following:

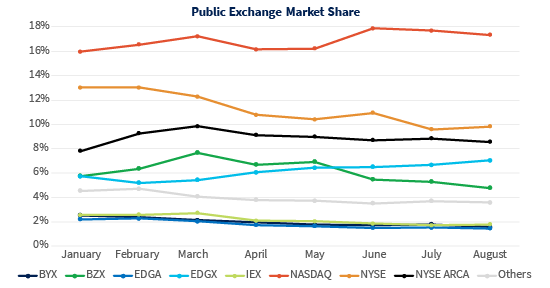

Public venues have historically averaged approximately 60% of total equity trading. Among public venues, five maker-taker exchanges (NASDAQ, NYSE, ARCA, Cboe BZX and Cboe EDGX) constitute most of this volume. These five destinations combined account for around 50% of the equity market. Another 10% is split between inverted venues and IEX. Although the Trade Reporting Facilities (TRF) percentages have increased to record highs, TRF market share hovers around 40% of equity trading. For a more in-depth look at this, see our detailed analysis of trading on off-exchange venues as reported via TRFs (1).

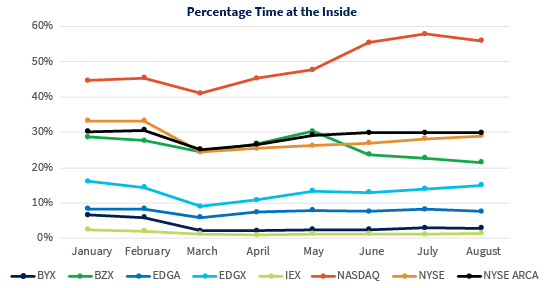

Time at the Inside

The increased number of active market centers in the U.S. equity markets means that there are typically several venues quoting on the inside of the consolidated National Best Bid or Offer (NBBO) at any given time. The average time on the inside for a venue is generally a function of two things: 1) the venue’s tendency to have ample liquidity in certain names; and 2) whether queue depletion rates are low, which means quotes remain active longer. When analyzing posted orders at a particular venue, time to first fill is an important factor to consider. Longer times at the inside may mean a longer wait to reach the front of the queue. These factors are worth considering when determining which market to post at, as market participants attempt to access the displayed quotes.

Figure 2 Average Time at the Inside (Bid or Ask) (3)

Figure 3 Average Time at the Inside by Tape (Bid or Ask) (4)

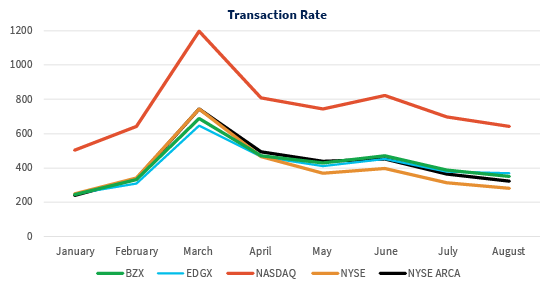

Transaction Rate

While being on the inside more frequently is generally a good sign for venues, it is equally important to analyze the conversion of time on the inside into transactions. Figure 4 below illustrates the transaction count during regular trading hours by exchange, normalized by time on the inside for venues with over 10% of time on the inside on average. EDGX stands out as one venue that showed notable relative improvement in transaction rates over the course of the year. Its transaction rate in August was ranked second as compared to fifth in January of this year. Even with a relatively lower time on the inside, EDGX showed a healthier transaction rate than peer exchanges. A higher transaction rate accompanied by lower time on the inside can indicate shorter queue times for posted orders. Therefore, when market participants attempt to reduce their opportunity cost for agency orders, EDGX may be a destination to include in their routing schema for evaluation with their Best Execution Committees.

Figure 4 Transaction Rate Per Second Normalized by Time on Inside During Regular Trading hours (5)

More Options = Better Execution?

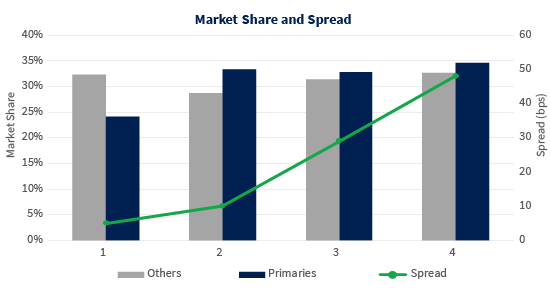

For market participants to benefit from increased venue competition, it is important to fully leverage this competition across various stock demographics. However, we typically see that not all symbols benefit from increased competition in the same manner. Narrowing spreads is an important measure that highlights competitiveness in a market. Spreads are generally the narrowest in the most heavily traded stocks. When studying fill distributions for the most liquid stocks, we found that during regular trading hours outside of the opening and closing of trading (09:35–15:45), these stocks trade across a broad range of venues, thereby leveraging the full spectrum of available destinations.

Figure 5 illustrates that spreads are the narrowest in the top quartile of stocks by liquidity. In the top quartile, primary venues represent about 24% of total volume versus 32% on the remaining public venues. As we move down the liquidity spectrum, spreads start widening and the primary listing venue market shares goes up to about 35%.

Figure 5 Spread and Market Share by Venue Type (09:35 -15:45) (6)

Since spreads are typically tighter for the most active tickers it is important for market centers to innovate and introduce new products that focus on different segments of the market. For example, the Periodic Auctions that we recently proposed to implement on Cboe’s BYX Exchange aim to provide increased competition in lower liquidity stocks that generally trade off-exchange at higher than average rates. As proposed, these auctions aim to enhance liquidity in tickers that are lightly traded and that may be underserved by the current competitive landscape, which primarily benefits trading in the most active names.

With 16 public market centers and multiple other options for trading, there is significant competition in the U.S. equity markets. It is prudent at this time to start quantifying the value of additional market centers, not just in terms of competition in the most liquid tickers, but in the broader universe of equity securities as well. In a world where visibility into public trading data is open to all participants, it is wise to evaluate the increase in the number of potential execution venues from a best execution lens. The incremental value for each new market center should also account for the broader market’s ability to provide competitive liquidity in names that are otherwise considered ‘difficult’ to trade.

Please do not hesitate to reach out with any questions on how Cboe can assist you with understanding your firm’s performance on our public exchanges along with other market centers. Cboe is prepared to review your trading data to assist you in satisfying your best execution obligations.

(1): Lighting Up the Dark

(2) — (6): Cboe Market Data

2020 Cboe Exchange, Inc. All rights reserved.

The information in this letter is provided for general education and information purposes only. No statement(s) within this letter should be construed as a recommendation to buy or sell a security or to provide investment advice. Supporting documentation for any claims, comparisons, statistics or other technical data in this letter is available by contacting Cboe Global Markets at www.cboe.com/Contact.