Read More

Dear Cboe Europe Participants and Members of the Trading Community,

Welcome to Cboe Europe’s Q2 Equities Newsletter, which summarises our activities over the last three months and looks ahead to our plans for the rest of the year.

Q2 Market Share Highlights

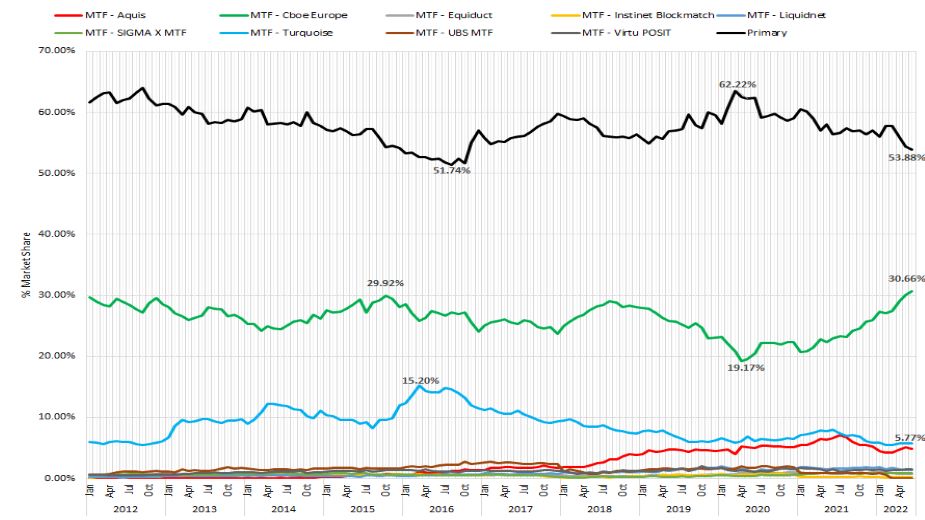

For Cboe Europe, it was a period of continued growth including some major milestones. Our overall market share reached 23.2% during the quarter, up from 21.9% in Q1. Our intraday market share (excluding Opening and Closing Auctions) grew to 29.9% during Q2, up from from 27.4% in Q1. This included a 30.7% intraday market share during June, a record monthly high and the highest combined market share since the launch of Chi-X Europe in 2007 and Bats Europe in 2008 (see chart below).

Primary versus MTF Intraday Market Share (excluding Open/Close)

Source: Cboe Global Markets

Product Updates

Cboe BIDS Europe, our European block trading platform, continued to take market share over the quarter and was the largest venue of its type for all three months in Q2. Its above-LIS market share was 32.7% in Q2, compared with 29% in Q1 (source: big xyt). Its above-LIS market share of 34% in May was a record high and comfortably ahead of its nearest rival.

Our focus remains on onboarding new customers, and we have a healthy client pipeline of buyside firms and additional sponsoring brokers.

Against the backdrop of a more stable regulatory environment and increasing optimisation of client interactions to our Periodic Auctions service, this mechanism continues to grow in adoption. As a venue grouping, they accounted for 5.6% of intraday activity during Q2, a record high and compared with 5.4% in Q1.

Cboe added additional functionality to its European Periodic Auctions in May, with the introduction of an Accept or Cancel (AOC) order type. AOC orders are evaluated upon receipt and are only accepted (and converted into a Good For Auction order) if there’s already a resting contra order and an execution is expected. Otherwise, they are immediately rejected, allowing the broker to move on to accessing other mechanisms. This order type allows brokers to utilise Periodic Auctions for urgent liquidity-taking flow, searching the venues for liquidity and/or price improvement prior to crossing the spread in lit markets. The AOC order type also allows Periodic Auctions to be used to capture passive liquidity. For every AOC order seeking far-touch (or just inside) liquidity in a Periodic Auction, there’s an opportunity to provide liquidity and capture the spread. Please contact us if you want more details on this new order type.

Regulatory Updates

Our recent advocacy efforts have focused on the negotiations among EU member states on the MiFIR review, with several encouraging developments emerging during the French Presidency of the European Council. On the topic of equity transparency, these include a proposal for ESMA to conduct a pilot scheme to help calibrate any minimum size threshold for Reference Price Waiver (RPW) venues. While we remain opposed to any further restrictions on RPW venues, a pilot of this type-- provided it was well designed and with clear success criteria-- would be a major step forward given our calls for regulatory decisions to be based on empirical data. If this is the approach taken, ESMA should be required to clearly evidence that any restrictions applied to RPW venues have improved investor outcomes by narrowing spreads and reducing investors’ transaction costs.

Positive amendments have also been tabled regarding an EU Equity Consolidated Tape (CT). We have strongly advocated for a real-time pre-trade and post-trade tape for many years and were disappointed with certain elements of the European Commission’s original proposals, which included a post trade-only CT and Regulated Markets being the sole beneficiaries of CT revenues.

Encouragingly, the French Presidency and European Commission have been actively exploring options for a more ambitious Consolidated Tape, including:

We recently collaborated with trade associations representing the biggest consumers of EU market data on a statement of principles for establishing an EU equity consolidated tape. These can be viewed here.

As always, thank you for your continued support and please let us know if you have any feedback on any of the above.

Natan and the Cboe Europe Equities Team