Global Markets

Tradable Products

Featured Products

On November 21, 2021 Cboe Options Exchange extended its existing Global Trading Hours (GTH) session and introduced a 24x5 trading model for S&P 500 Index (SPX and SPXW) and Cboe Volatility Index® (VIX® Index) options. Market participants will now be able to trade or hedge broad U.S. market and global equity volatility conveniently across all time zones, nearly 24 hours a day, five days a week.

The expanded trading hours will enable market participants to react quickly to market moving events, access U.S. index options globally and develop new trading strategies to diversify and hedge their portfolio. To highlight the benefits of 24x5, we explore extended GTH use cases and trading strategies for VIX and SPX options below.

SPX options and VIX options and futures have the potential to be powerful tools for market participants who wish to manage or adjust their exposure.

Over a period of 20 trading days in early 2020, the S&P 500 Index fell 25.3%, while the March 18 VIX futures rose 358% and the VIX March 20 call options rose 6393%. These gains were unusually strong and there may be losses involved with the purchases of the futures and options.

Source: Cboe Global Markets

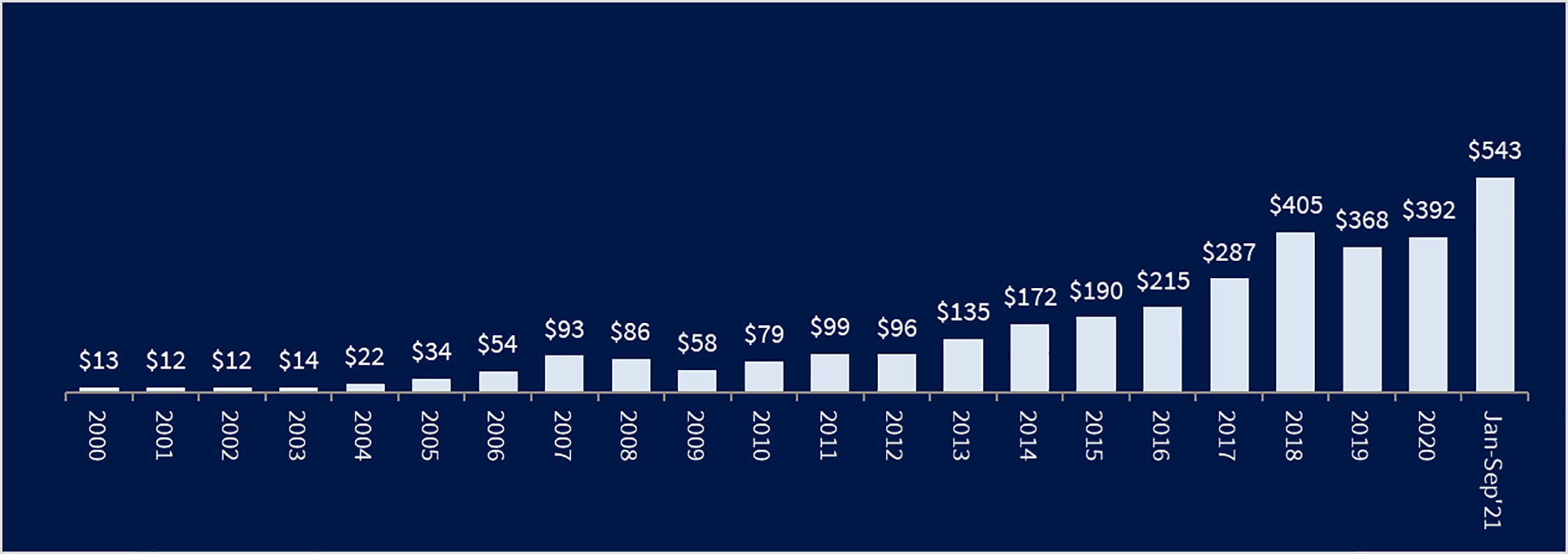

Institutional investors often prefer larger notional sizes for trading instruments to be used. In recent months the notional value covered by one SPX options contract has typically been above $400,000, and in 2021, the average daily notional value of SPX options trading volume has been around $540 billion.

Rough estimates of notional volume in billions. Some analysts use a delta-weighting multiplier to develop more conservative estimates. Figures include both A.M.-settled SPX options and P.M.-settled SPXW options. Source: Cboe Global Markets

The charts below show the estimated 30-day volatility skew for SPX options and for VIX options on March 16, 2020, when the VIX Index hit its all-time daily closing high of 82.69, and on Oct. 22, 2021, when the VIX Index closed at 15.43. On Oct. 22, 2021, the out-of-the-money puts for the SPX options and the out-of-the-money calls for the VIX options were the highest implied volatilities for each contact.

STRATEGY IDEA | Market participants who are intrigued by the negative skewness often shown by stock index options may find utility in the Vertical Put Spread strategy, which involves selling a put and simultaneously buying another put at a different strike price, but with the same expiration.

Source: Cboe Global Markets

Source: Cboe Global Markets

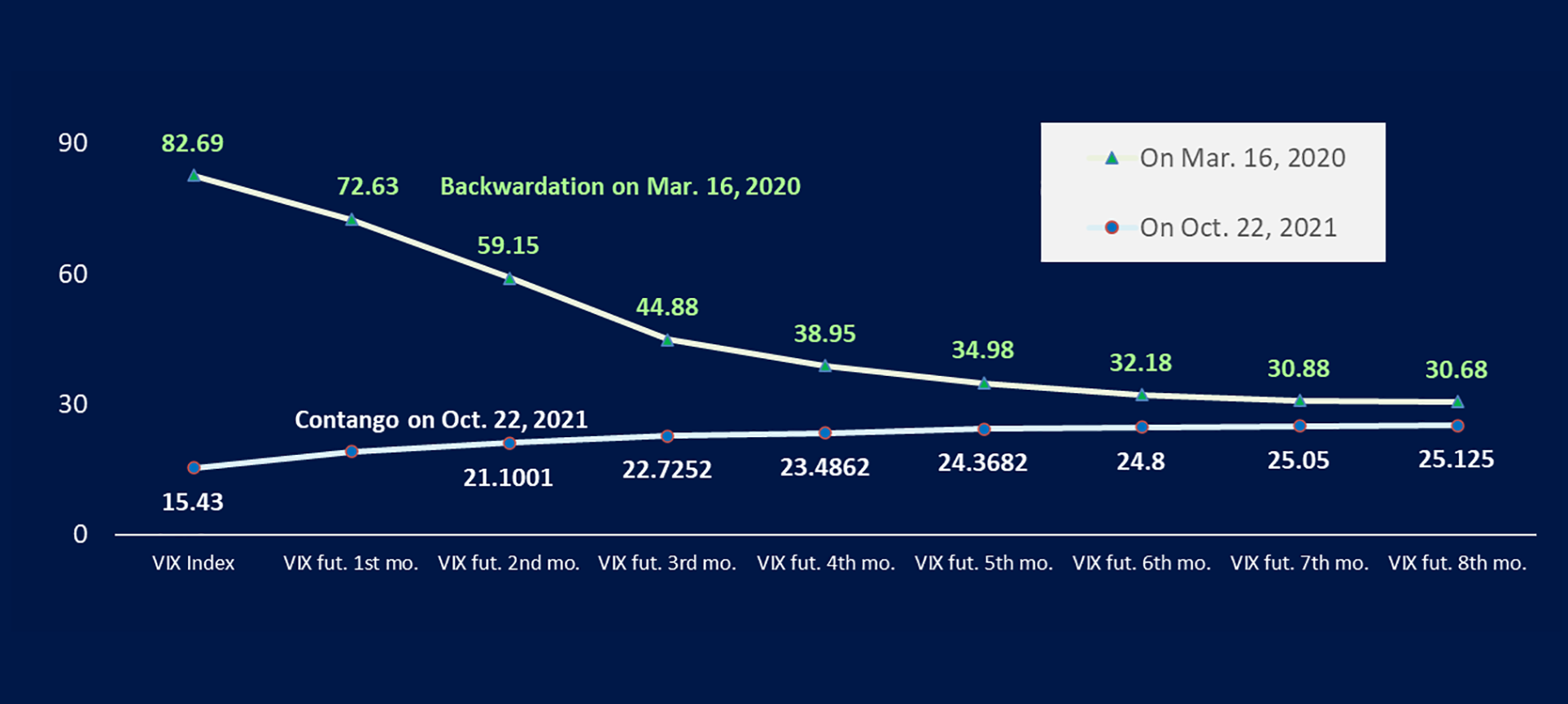

The VIX Index was in backwardation on March 16, 2020 when the VIX Index reached an all-time daily closing high of 82.69, and was in contango on October 22, 2021. The VIX Index has a tendency to be mean-reverting and has been in contango on most trading days since the launch of VIX futures in 2004.

With expirations from October 27, 2021 through December 15, 2023. The S&P 500 Index closed at 4544.9 on October 22, 2021.

Source: Cboe Global Markets

The SPX options term structure shows higher implied volatilities for the near-term out-of-the-money SPX options puts, which often are purchased for equity portfolio protection. In light of the higher implied volatilities, some sophisticated investors may sell short-dated cash-secured SPX options puts.

With expirations from October 27, 2021 through June 22, 2022. The VIX Index closed at 15.43 on October 22, 2021.

Source: Cboe Global Markets

The VIX options calls with the highest implied volatility were the near-term out-of-the-money VIX options 20 calls, which are purchased by participants who want trading instruments with potential to rise during steep equity market corrections.

Source: Cboe Global Markets

STRATEGY IDEA | Options investors who expect a change in a steep term structure in the near future may leverage the calendar spread strategy, which involves the buying and selling of a call option (or the buying and selling of a put option) with the same strike price but with different expiration dates.

Cboe offers dozens of benchmark indices designed to track the performance of hypothetical strategies that use options. Interest in strategies that can help manage left tail risk and mitigate portfolio drawdowns has increased since the start of the COVID-19 pandemic. As illustrated in the chart below, two Cboe benchmark indices that buy index options outgained some major traditional benchmark indices from year-end 2019 through October 21, 2021. The Cboe VIX Tail Hedge Index (VXTHSM) bought VIX call options and rose 137%, while the Cboe S&P 500 5% Put Protection Index (PPUTSM) rose 48%.

Source: Cboe Global Markets

For decades investors have sold stock index options with goals of receiving options premiums and generating enhanced risk-adjusted premiums. The average of the monthly gross premiums as a percentage of the underlying for theCboe S&P 500 PutWrite Index (PUTSM), which sells cash-secured at-the-money SPX options puts, was 1.9% and 0.8% for the Cboe S&P 500 2% OTM BuyWrite Index (BXYSM), which sells out-of-the-money SPX options calls. At-the-money option writing strategies often collect more premium and have less equity upside participation when compared to out-of-the-money option-writing strategies.

May 2006 - October 2021. The amounts shown are for gross premiums received and the net returns for the strategy can be less or negative. *Gross amount of premiums received as a percentage of the underlying.

Source: Cboe Options Exchange

The Sortino Ratios chart shows that since mid-1986 three Cboe benchmark indices that sell SPX options - PUT, BXMDSM, and CMBOSM – all had higher risk-adjusted returns, as measured by the Sortino Ratio, than some key traditional benchmark indices.

Total return pre-tax indices. Source: Zephyr and Cboe Global Markets

There are a number of strategies and use cases to explore when trading SPX and VIX options during extended global trading hours. With more time to trade, market participants will be able to react quickly to market moving events, access U.S. index options globally and develop new trading strategies to diversify and hedge their portfolio.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at https://www.cboe.com/options_futures_disclaimers