Global Markets

Tradable Products

Featured Products

Life is Better with Options.®

Your investments could be too.

Discover more options for your portfolio.

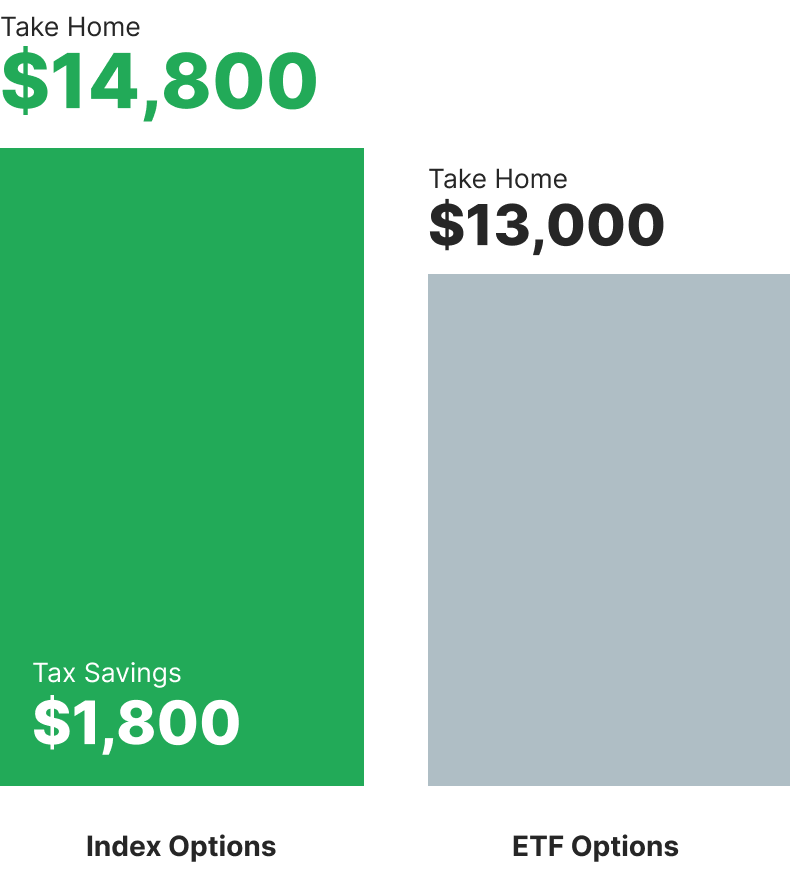

More profit or more taxes?

Some choices are easy to make. Cboe Index Options may qualify for certain tax advantages that keep more profit in your pocket.

Index options are 1256 contracts, *which means they qualify for 60/40 tax treatment – meaning 60% of your profits are treated as long-term capital gains and 40% as short-term capital gains.

Use the dropdown to see how much you could potentially take home with Cboe Index Options vs. ETF Options.

$20,000

Assumes that the investors in the index option and the ETF option are both in the 35% tax bracket and filing jointly, with a long-term capital gains tax rate of 20%.

Large. Medium. Small.

More contract sizes give you more control.

Cboe Index Options let you access flexible contract sizes. This includes contracts with smaller values that may be a better fit for traders' goals and account sizes.

Cash money? Yep. That’s an option.

Index options are settled in cash at expiration. That means your trade’s profits and losses are settled as a debit or credit directly into your trading account. So now you don’t have to worry about receiving or delivering shares upon exercise or assignment.

Cash Settled

NOT Cash Settled

Stay up to date on education, trading resources and news.

Stay informed about the latest products and market insights.

Ready for more options?

If you want to take a deeper dive into the ins and outs of Cboe Index Options, we have a great resource for you. Our comprehensive guide gives you more details about the world of options available to you with these products.

* Under section 1256 of the Tax Code, profit and loss on transactions in certain exchange-traded options, including SPX Options, are entitled to be taxed at a rate equal to 60% long-term and 40% short-term capital gain or loss, provided that the investor involved and the strategy employed satisfy the criteria of the Tax Code. Investors should consult with their tax advisors to determine how the profit and loss on any particular option strategy will be taxed. Tax laws and regulations change from time to time and may be subject to varying interpretations.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/global-disclaimers/.