Data Analytics and Indices

This article is part of our three-part series: “How to Utilize Cboe’s S&P 500 Index Options Benchmark Indices,” which highlights the hedging, income-generation and spread strategies investors may explore, with analysis of more than 35 years of data history of Cboe’s benchmark indices. Read part one, “Hedging Downside Exposure with PPUT, CLL and CLLZ Indices” and part two, “Income Generation and Smoother Returns with Cboe’s BXM, BXMD, PUT and CMBO Indices” on Cboe Insights.

When the Cboe SKEW Index (SKEWSM) hit an all-time high of 170.55 in late June, it became clear that many investors were concerned about volatility and downside risk of the U.S. stock market. The data history for the SKEW Index begins in 1990, and its record high value this year shows there is currently strong demand for hedging against big losses in S&P 500 Index portfolios.

Investors who are concerned about downside risk and want to limit downside moves, but think the stock market probably will trade within a narrow range in the near future may find utility in, the iron condor and iron butterfly strategies. Two of Cboe‘s benchmark indices – the Cboe S&P 500 Iron Condor Index and the Cboe S&P 500 Iron Butterfly Index -- track these strategies and have more than 35 years of performance history to prove their efficacy.

The CNDR Index is a benchmark index designed to track the performance of a hypothetical option trading strategy that:

The profit-and-loss diagram below shows that the gains and losses for the CNDR Index should be limited as the stock index moves up or down, enabling investors to manage volatility through this strategy.

The histogram below shows the ranges of monthly returns over 35 years. The CNDR Index had fewer monthly increases or decreases of more than 6% than the S&P 500 Index. Additionally, 59% of the time, the CNDR Index had returns between 0% and 2%.

Source: Cboe Exchange, Inc.

The BFLY Index is a benchmark index designed to track the performance of a hypothetical options trading strategy that:

Similar to the CNDR Index profit-and-loss diagram, the profit-and-loss diagram below illustrates that the gains and losses for the BFLY Index should limited as the stock index moves up or down.

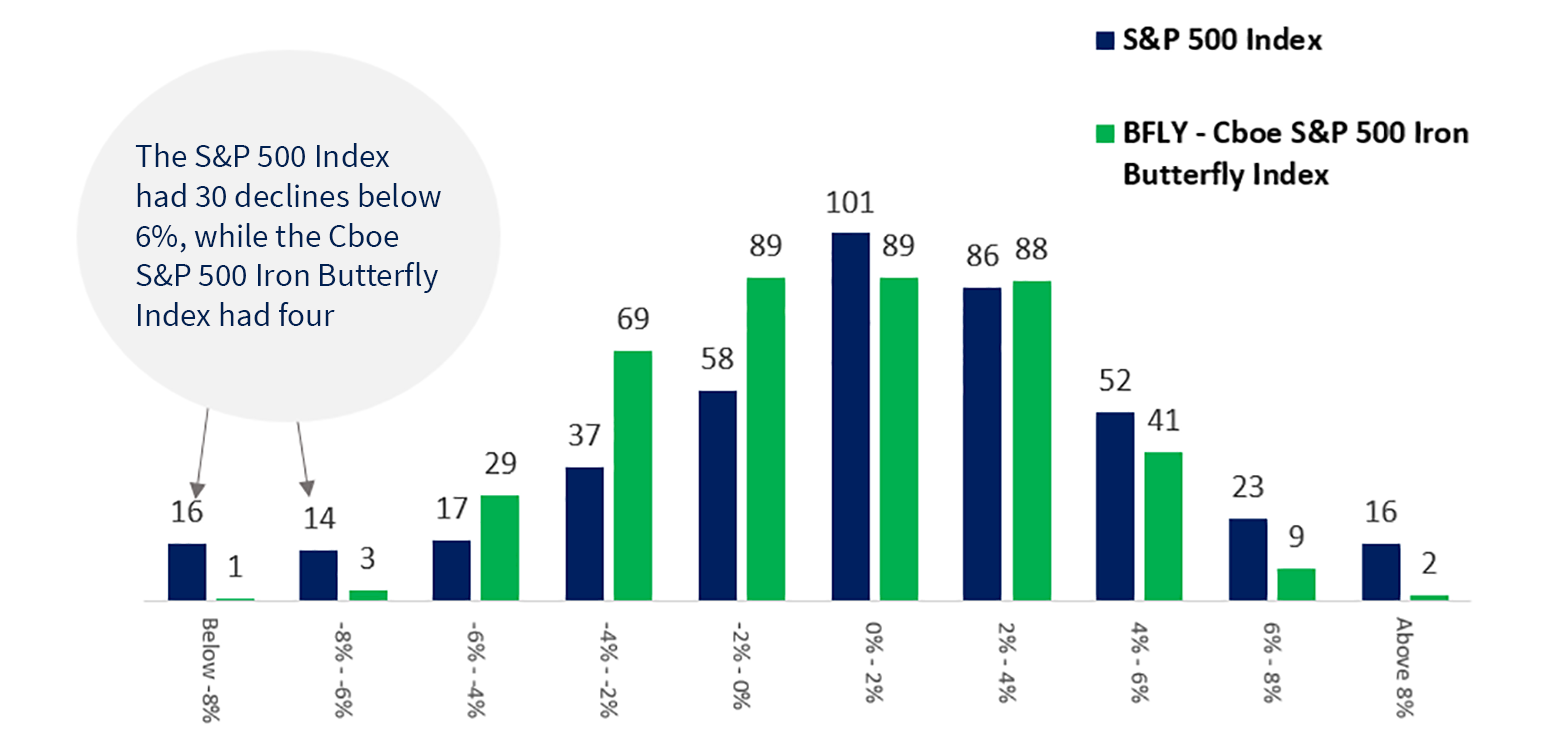

The histogram below shows the ranges of monthly returns over 35 years. The BFLY Index had fewer monthly increases or decreases of more than 6% than the S&P 500 Index. The BFLY Index helps investors access the S&P 500 Index, without taking on some of the associated risk.

Source: Cboe Exchange, Inc.

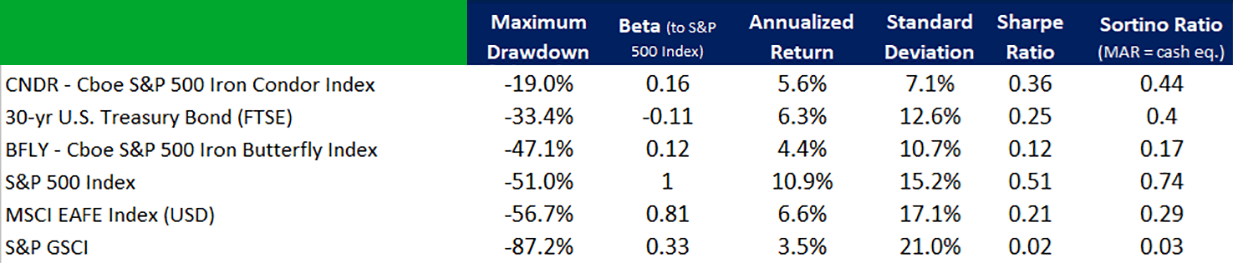

Many risk-averse investors seek to limit peak-to-trough drawdown losses. Over the past 35 years, the CNDR Index and BFLY Index had lower maximum drawdown losses than the S&P 500 Index. The worst peak-to-trough monthly drawdown losses were 19% for the CNDR Index and 47.1% for the BFLY Index, compared to 51% for the S&P 500 Index.

Sources: Zephyr and Cboe Options Institute

Since 1986, the S&P 500 Index has only experienced increases or decreases of more than 10% in 11 months. In those 11 months, neither the CNDR nor the BFLY indices rose or fell by 10% or more.

Throughout their performance history, Cboe’s BFLY and CNDR indices had:

The CNDR and BFLY indices may be worth exploring for risk-averse investors who are looking to diversify their investment portfolios and manage volatility.

Raj Shah and Philip Markuszewski, summer 2021 interns on Cboe’s Options Institute and Derivatives Strategy teams, contributed to this report.

The information in this article is provided for general education and information purposes only. No statement(s) within this article should be construed as a recommendation to buy or sell a security or to provide investment advice. Supporting documentation for any claims, comparisons, statistics or other technical data in this article is available by contacting Cboe Global Markets at www.cboe.com/Contact. Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of “Characteristics and Risks of Standardized Options.” Copies are available from your broker or from The Options Clearing Corporation at 125 South Franklin Street, Suite 1200, Chicago, IL 60606 or at www.theocc.com. Past Performance is not indicative of future results. Cboe is a registered trademark of Cboe Exchange, Inc. All other trademarks and service marks are property of their respective owners. © 2021 Cboe Exchange, Inc. All Rights Reserved.

The Cboe S&P 500 Iron Condor Index (CNDR) and Cboe S&P 500 Iron Butterfly Index (BFLY) (the “Indexes”) are designed to represent proposed hypothetical options strategies. The actual performance of investment vehicles such as mutual funds or managed accounts can have significant differences from the performance of the Indexes. Investors attempting to replicate the Indexes should discuss with their advisors possible timing and liquidity issues. Like many passive benchmarks, the Indexes do not take into account significant factors such as transaction costs and taxes. Transaction costs and taxes for strategies such as the Indexes could be significantly higher than transaction costs for a passive strategy of buying-and-holding stocks. Investors should consult their tax advisor as to how taxes affect the outcome of contemplated options transactions. Past performance does not guarantee future results. It is not possible to invest directly in an index. Cboe Global Indices, LLC calculates and disseminates the Indexes.