Data Analytics and Indices

Exchange Traded Funds (ETFs) linked to BuyWrite℠indices have grown significantly in the U.S. in recent years. Income-focused ETFs — where BuyWrite strategies represent a significant share — reaching approximately $81 billion in assets under management (AUM) by 2024, according to Global X. The growing interest in the U.S. has begun to spill over to other regions as global investors see opportunities to implement similar strategies.

Two new indices developed by Cboe Global Indices target Japanese exposure to the BuyWrite strategy – the Cboe® TLT 2% OTM BuyWrite Index JPY (BXTBJPY) and the Cboe® S&P 500® Enhanced 1% OTM BuyWrite NTR Index JPY (BXVBWJPY).

Income Generation and U.S. Market Access: Both BuyWrite indices are designed to help investors earn more income by selling call options on their respective underlying ETFs – in this case, iShares® Core S&P 500 ETF (IVV) (S&P 500) and iShares® 20+ Year Treasury Bond ETF (TLT) (U.S. treasury bonds). With interest rates in Japan remaining relatively low, this approach offers Japanese investors a way to potentially increase returns for their portfolios while gaining exposure to U.S. markets.

Out-of-the-Money (OTM) Strategy: While there are some BuyWrite (covered call) U.S. equity indices already listed in Japan, selling call options on OTM strikes offer different dynamics to selling at-the-money (ATM) options. Although OTM options generate smaller premiums than ATM options, they offer a better chance of keeping those premiums if markets rally, allowing investors to benefit from both income and potential growth.

First BuyWrite Index on TLT in Japan: This is the first time ETF BuyWrite strategies on U.S. Treasury bonds (via TLT) have been targeted to Japan. It gives Japanese retail investors a new way to express views on the U.S. bond market while aiming to enhance income.

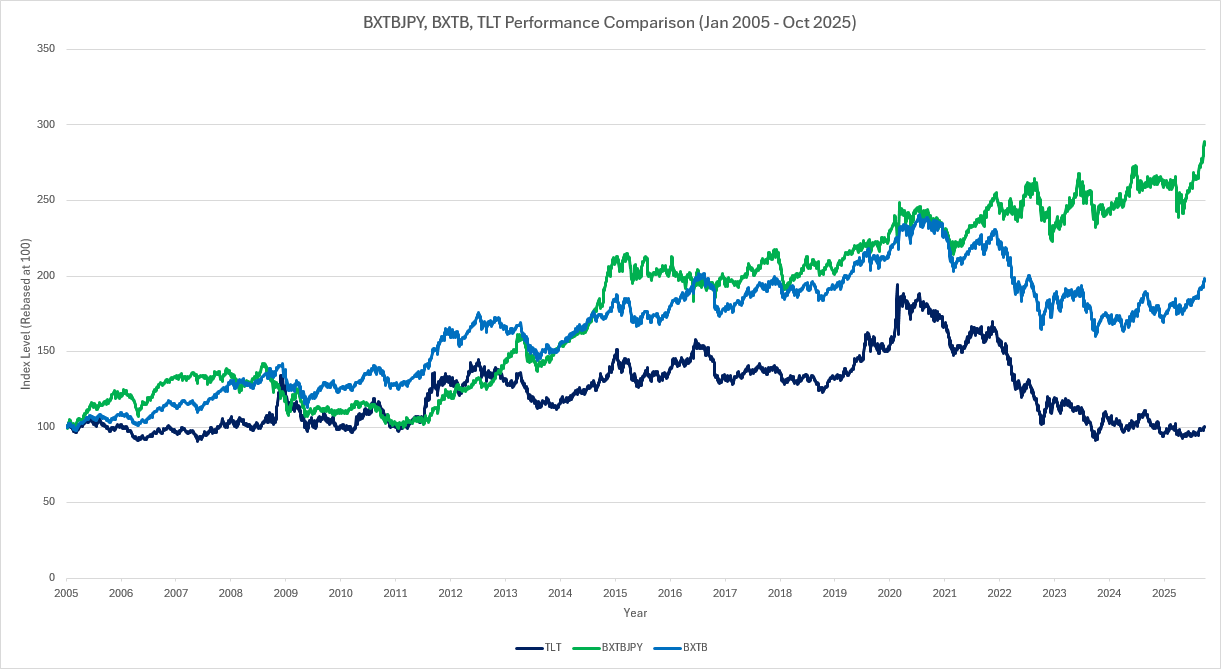

BXTBJPY measures the performance of the net total return version of the BXTB Index in Japanese Yen. It tracks a covered called strategy involving a long position on the iShares® 20+ Year Treasury Bond ETF (TLT) and short monthly out-of-the-money call options on the underlying asset.

Figure 1: Performance of TLT and BXTBJPY from January 2005 to October 2025 rebased at 100

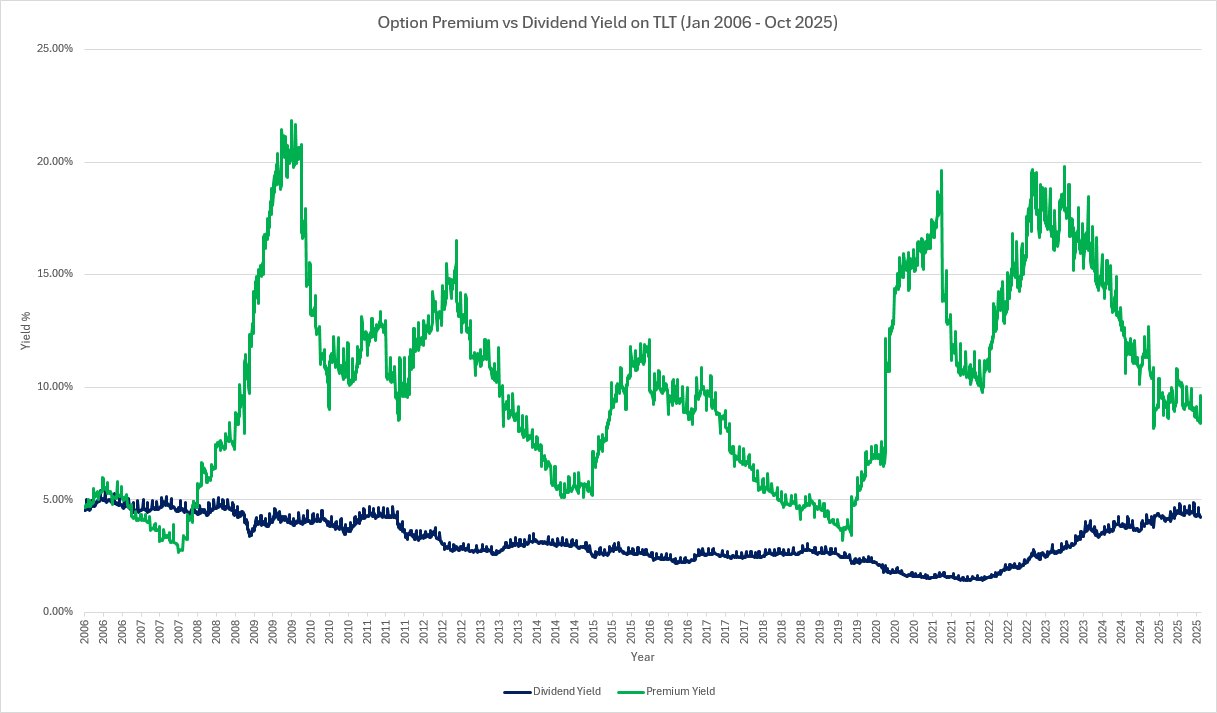

Figure 2: Dividend yields from TLT versus the yields generated through selling call options on TLT over the period from January 2006 to October 2025

By systematically generating premiums through selling monthly call options on TLT, BXTBJPY delivered a significantly higher total income compared to TLT alone, whose returns were limited to dividend distributions. A covered call strategy would receive the dividend yield and the premium yield.

Figure 3: Financial metrics comparison between TLT and BXTBJPY from January 2005 to October 2025

Following the COVID-19 pandemic, the U.S. experienced a period of rapid rate hikes and the onset of quantitative tightening triggered a sell-off in long duration U.S. Treasury bonds. In this environment, a covered call strategy on TLT proved more effective, benefiting from elevated option premiums due to increased volatility in the bond market and more consistent premium capture.

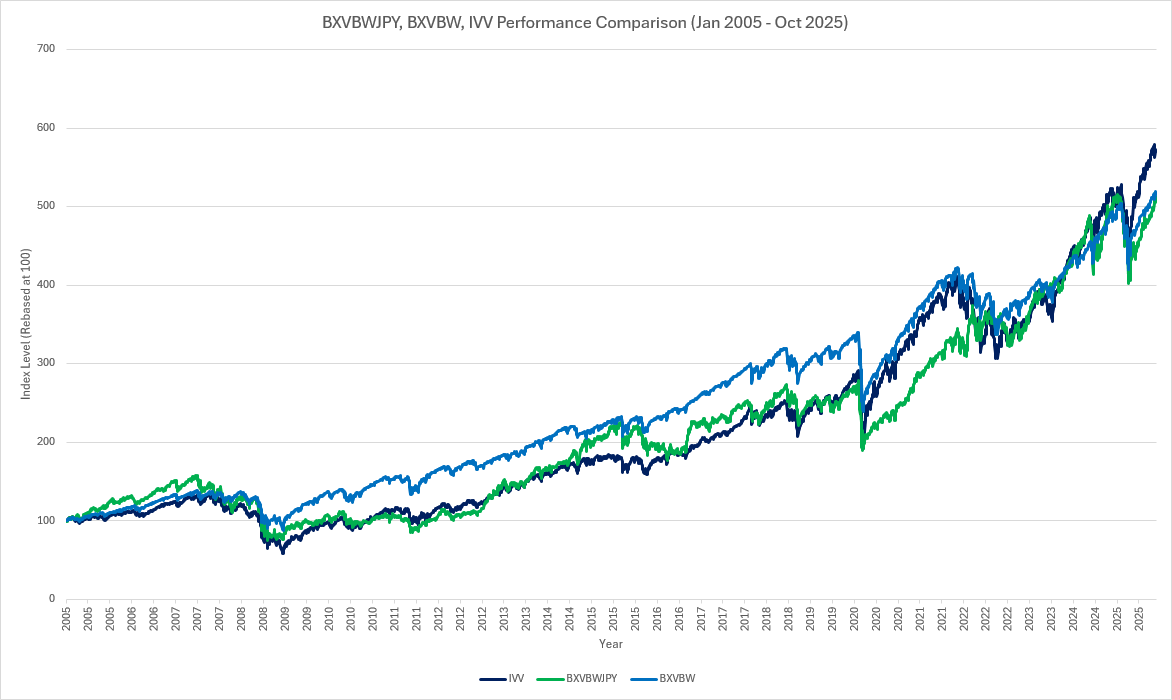

BXVBWJPY measures the performance of the net total return version of the BXVBW Index in Japanese Yen. The BXVBW Index tracks a covered call strategy involving a long position in the iShares Core S&P 500 ETF (IVV) overlayed with a monthly short SPX® out-of-the-money call option.

Figure 4: Performance of IVV and BXVBWJPY from January 2005 to October 2025 rebased at 100

While a covered call strategy on the S&P 500 Index may underperform the index in a strong bull market, it can generate additional income that helps cushion losses if the market turns downward.

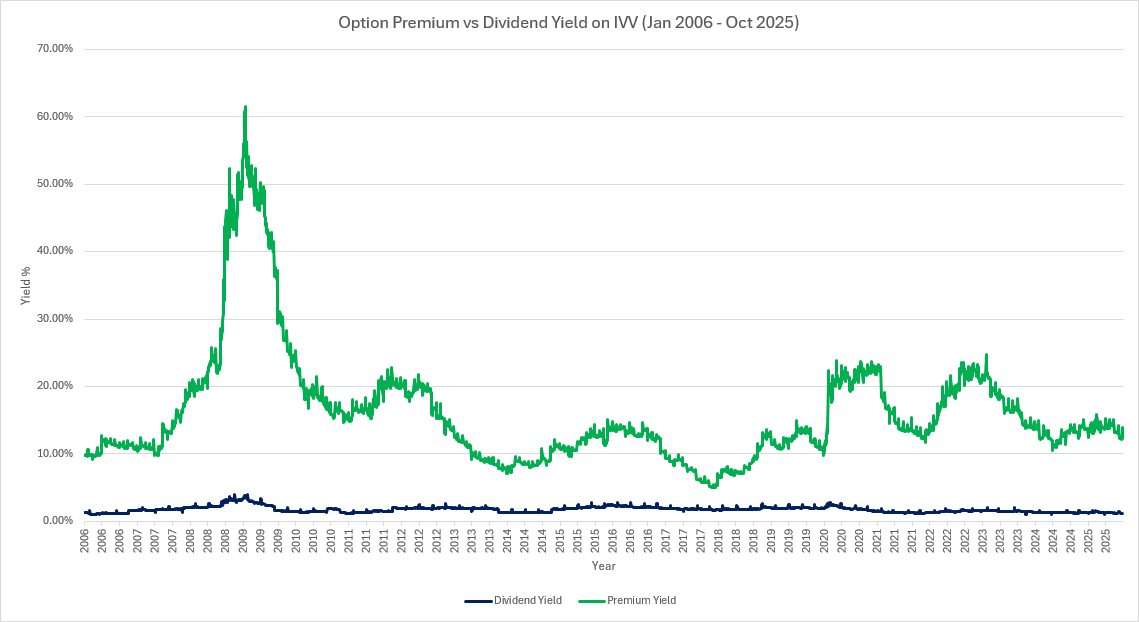

Figure 5: Dividend yields from IVV versus the yields generated through selling call options on IVV over the period from January 2006 to October 2025

This indicates how selling options can potentially boost income particularly during stressed periods when premiums are high. These are typically the periods when covered call strategies can outperform the underlying asset. However, this enhanced income may come at the cost of reduced upside potential from capital gains.

Cboe brings deep expertise in building option-based indices, and these new offerings provide a compelling new solution for the Japanese market, seeking additional yield in a low-rate environment.

The information herein is provided solely for informational purposes. Past performance of an index or financial product is not indicative of future results. Indices are not financial products that can be invested in directly, but they can be used as the basis for financial products (for example, without limitation, options, futures, mutual funds or exchange-traded funds) or to help manage portfolios. Nothing herein should be construed as investment advice.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/global-disclaimers/. These products are complex and are suitable only for sophisticated market participants. In certain jurisdictions, Cboe Company products are only permitted for investment professionals, certified sophisticated investors, or high net worth corporations and associations. These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position. Market participants should put at risk only funds that they can afford to lose without affecting their lifestyle. © 2025 Cboe Exchange, Inc. All Rights Reserved.