Macro volatility declined last week following the Fed meeting, even as Powell injected more uncertainty into the December meeting. Both rates and FX volatility fell to a 1-year low following the FOMC, while gold volatility continued to normalize. In contrast, equity and credit volatilities increased wk/wk, with the VIX® index gaining 1.0 pt despite the market rally as SPX® fixed-strike vols increased (aka "spot up, vol up").

SPX skew flattened further last week, as hedgers capitulated and call demand increased. The decline in skew over the past two weeks has been notable: SPX 1M skew has fallen from the 99th percentile high three weeks ago to a low of 6th percentile earlier last week, before ending the week at the 48th percentile. Longer-dated skew screens even cheaper, with SPX 6M skew now in the 16th percentile low.

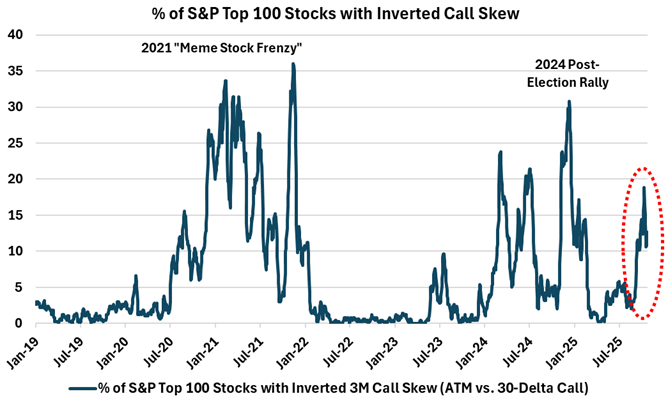

The flattening in index skew is consistent with the pickup in bullish sentiment we’ve observed in single stock options. The number of stocks in the S&P top 100 trading with inverted call skew (a sign of extremely bullish sentiment) has surged to a high of 20% (vs. historical average of just 3%). While the metric is not yet at the extremes we saw in 2021 or late last year, it certainly signals a high level of investor optimism going into year-end.