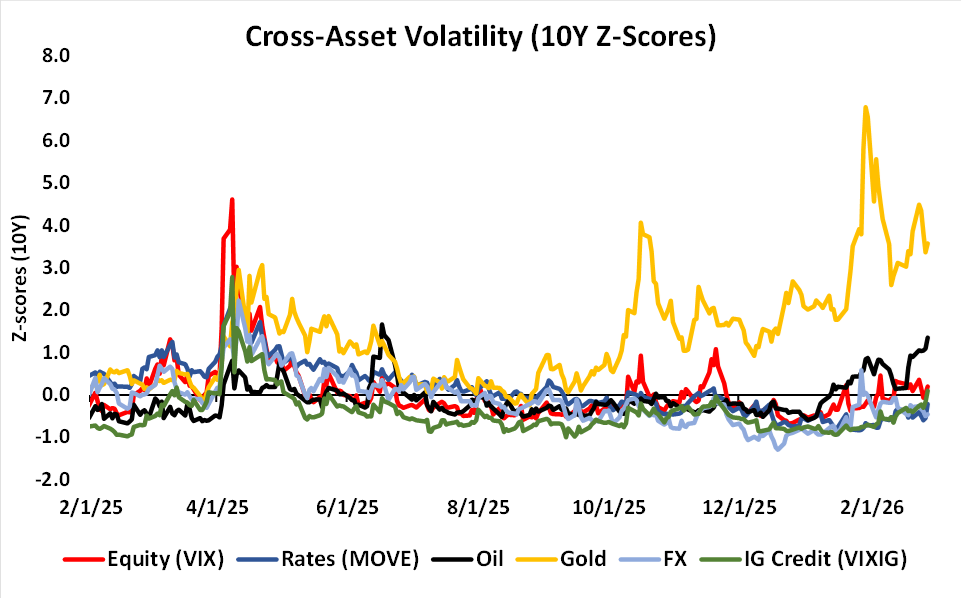

Implied volatilities are up across asset classes following the US/Israeli strikes on Iran over the weekend. Oil 1M implied volatility jumped 7 pts as oil prices spiked, with skew remaining extremely inverted (i.e. upside bid). As we noted last week, what’s unusual about this latest geopolitically-driven spike in oil prices is the positioning in long-dated oil options. While it’s not uncommon to see skew invert at the front-end of the curve, we’re seeing this extend to 6M options as well which hasn’t happened since the 2022 Russia/Ukraine war. Aside from geopolitics, we also saw a notable bid to credit volatility last week on the back of rising private credit fears, with VIXIG index gaining 10 pts wk/wk. For most of the past year, credit volatility has traded as the cheapest cross-asset vol, but that has changed in recent weeks (see chart below). Rates and FX vols now screen as the cheapest.

The VIX® index is up almost 4 pts this morning, outperforming the sell-off in S&P futures (-1.1%). This is on the back of higher SPX® fixed-strike vols (contributing 1.8 VIX pts) and steeper skew/convexity (contributing another 0.7 pt to the VIX index). As we’ve highlighted in recent weeks, SPX skew has steepened significantly this year on the back of increased hedging demand, with 1M skew now nearing the Aug-2024 yen carry unwind extremes.

Despite being a new product (launched in Dec), Cboe® Magnificent-10 Index (ticker: MGTN) options have seen increasing interest from investors looking for a targeted way to trade the AI/tech theme. Almost 40k contracts traded on Friday (~$1.6B notional), with the vast majority of the volume concentrated in the 3/3 expiry (2DTE) 381-386 puts (5-7% OTM). Flow, however, was fairly balanced between buys vs. sells.