Global Markets

Tradable Products

Featured Products

Guest Author: Euan Sinclair, Senior Financial Engineer, Hull Tactical Asset Allocation

There are two very consistent flows into the options markets. People buy puts as insurance and people sell calls against stock holdings. As a result, index put options are more expensive, reflecting structural demand for insurance. Conversely, covered-call strategies continually add supply of calls, pushing implied volatilities on the upside lower. These flows can create opportunities for traders who are price-sensitive and adaptive.

But these strategies don’t aim to maximize return.

The purpose of these strategies is to provide downside cover, smoother return profiles, to trade some upside for less downside, or to transform volatile equity exposure into a more income-like stream. Those are legitimate goals for many investors.

However, these are not the goals of a fund that seeks risk-adjusted outperformance. A portfolio built to truly maximize Sharpe ratio will adapt to market conditions and only take exposures when the expected compensation exceeds the risk.

Hull Tactical’s options strategy strives to maximize risk-adjusted returns — to deliver excess performance with market-like volatility. We trade around core positions, adjusting exposures as markets and option prices evolve. And in doing so, we benefit from the price distortions that may be created by passive, rule-based funds.

When large investors pay for puts, someone else collects that excess premium. When covered-call sellers depress call prices, those calls can become attractive buys for investors seeking convexity at a discount. The mechanical behavior of these ETFs effectively subsidizes liquidity and creates edge for anyone willing to take the other side with discipline and valuation awareness.

One simple, intuitive way to capture this opportunity is through the risk-reversal — a classic options structure that involves buying a call and selling a put on the same underlying, typically at similar deltas (for example, both 25-delta).

In equity terms, this is a long delta position — it benefits when the market rises, much like owning stock. But that’s not the main reason to hold it. Stock can provide delta exposure more cheaply and without the complexities of options. The reason to use options is that they offer exposure to volatility as well as direction.

The risk-reversal takes advantage of the relative mispricing between puts and calls. You’re selling something that’s typically expensive (the put) and buying something that’s typically cheap (the call). If you believe volatility will remain stable or decline, and you can value these options sensibly, this trade carries positive expected value.

If you cannot forecast volatility, then this exposure is a source of unwanted risk. But if you can measure and anticipate it — even modestly — that volatility edge compounds over time.

When we isolate the volatility component of this strategy, it has historically been profitable, with a Sharpe ratio higher than simply holding the S&P 500. That finding is intuitive: you are systematically selling overpriced downside volatility and buying underpriced upside exposure.

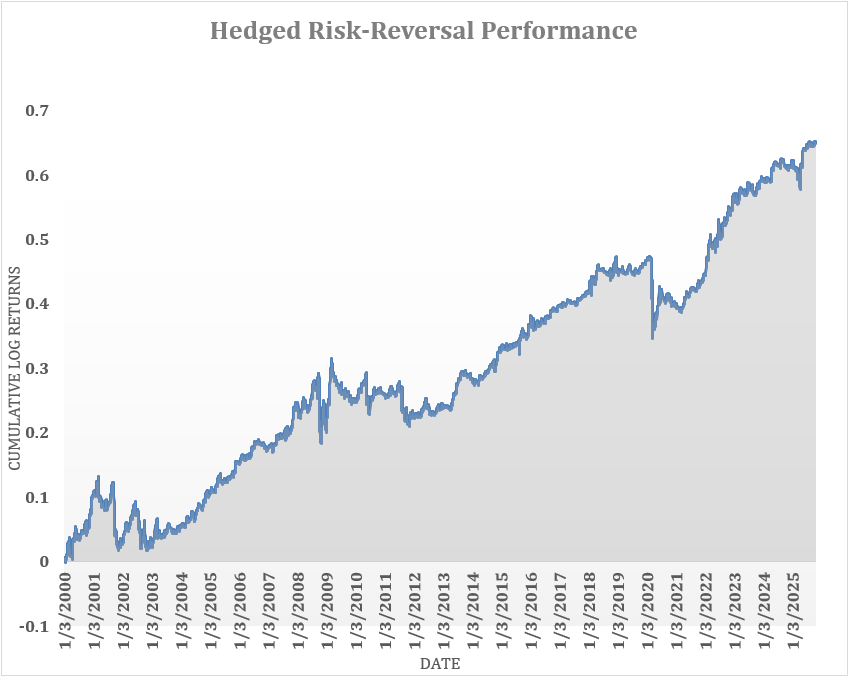

To illustrate, consider the Cboe RXM Index. This benchmark implements a straightforward monthly risk-reversal: each month it sells a 25-delta SPX put and buys a 25-delta SPX call, and holds the position until expiration.

If we delta-hedge that strategy — neutralizing the directional exposure so we measure only the volatility effect — the results are instructive:

Source: Hull Tactical

Compound Annual Growth Rate: 2.5%

Volatility: 5.4%

Information Ratio: 0.47

That may not sound that impressive, but compare it to a buy-and-hold S&P 500 position over the same period, which has an information ratio of about 0.31. More importantly, the returns come from exposure to a different risk factor — volatility risk — making it a useful source of diversification in a broader portfolio.

Option markets, especially in equity indices, have a well-documented tendency toward downside skew: investors are willing to overpay for protection and underpay for upside. This is partly behavioral and partly structural, because institutional mandates often require hedging but not speculation.

As a result, volatility has become not just a measure of risk, but a tradable asset class with its own supply and demand dynamics. Investors who understand those dynamics and are willing to be liquidity providers when the crowd demands insurance could earn a structural premium.

For Registered Investment Advisors, the practical takeaway is not that every client portfolio should include exotic option trades. Rather, it’s to understand what the popular option-based strategies are doing or not doing.

When you buy puts, you are paying for insurance. When you sell calls, you are giving away upside in exchange for current yield. Those may be entirely appropriate allocations depending on the investor’s want and need. But they are not sources of alpha, and they are not substitutes for a genuinely active, risk-managed approach.

The appeal of “derivative income” or “downside capped” strategies are emotional as much as financial. Investors like the feeling of collecting income and avoiding losses. Yet, as with any insurance product, the premium you pay (or forego) determines your long-term outcome.

Advisors who understand volatility as a priced risk factor — like credit or duration — may be better equipped to evaluate these trade-offs. Volatility exposure can be harvested intelligently, just as yield can. But it must be done selectively and with disciplined valuation.

Our approach is straightforward: remain long delta to participate in market growth, but adjust option exposures dynamically based on relative pricing and implied volatility. When downside puts are rich and upside calls are cheap—as they often are—we favor the risk-reversal structure. When the skew flattens or reverses, we scale back.

This flexibility distinguishes a truly active strategy from one that simply automates a risk preference. The goal is not just smoother returns but better returns per unit of risk — what every advisor ultimately seeks for clients.

By being willing to take the other side of price-insensitive flows, strategies like the risk-reversal can harvest the volatility premium those flows create. The trade may be simple — long a call, short a put — but the principle is profound: in markets, value accrues not to those who fear volatility, but to those who understand and price it.

Euan Sinclair is an option trader with nearly 30 years of professional trading experience. He currently manages the volatility exposures at Hull Tactical. Prior to joining Hull, he ran a long/short equity volatility book at Bluefin Trading. He was also the founder and CEO of FactorWave, a fintech company that provided factor-based portfolios to RIAs.

He holds a PhD in theoretical physics from the University of Bristol and has written six books including "Volatility Trading”, “Option Trading" and “Positional Option Trading” all published by Wiley. He is a member of the editorial board of the Journal of Investment Strategies, a publication of Risk Journals, and has written several papers on options, volatility and bet sizing.

Disclaimers:

All table and chart data is publicly available data from Cboe.

This article is part of Cboe’s Guest Author Series, where firms and individuals share their insights, strategies and ideas with the broader Cboe community. Neither Hull Tactical Asset Allocation's investment advisor registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved. A copy of Hull Tactical Asset Allocation's current written disclosure and Form CRS continues to remain available upon request at www.hulltactical.com.

The comments, opinions, data, and analyses expressed herein are for informational purposes only and should not be considered individual advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions, data, and analyses are rendered as of the date of this report and may change without notice. The information contained herein is not guaranteed as to accuracy or completeness. All performance data are historical and do not guarantee future results.

This commentary is not intended for the giving of investment recommendations to any single investor or group of investors, and no investor should rely upon or make any investment decisions based solely on its contents. All returns are shown net of fees. The indices shown are for informational purposes only and are not reflective of any investment. As it is not possible to invest in the indices, the data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. As it is not possible to invest in an index, the information shown does not reflect the features of an actual investment, such as objective, cost and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. The Strategy involves risk, including the possible loss of principal. There is no assurance that the Strategy will achieve its investment objectives. The use of leverage embedded in written options will limit the Strategy's gains because the Strategy may lose more than the option premium received. Selling covered call options will limit the Strategy's gain, if any, on its underlying securities, and the Strategy continues to bear the risk of a decline in the value of its underlying stocks. The S&P 500® Index consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market value-weighted index (stock price times the number of shares outstanding), with each stock's weight in the Index proportionate to its market value. It is widely used as a benchmark of U.S. equity performance. Standard deviation is a statistical measurement of volatility risk based on historical returns.

Investments in options involve risks different from, or possibly greater than, the risks associated with investing directly in the underlying securities. The S&P 500® Index is a capitalization-weighted unmanaged index of 500 widely traded stocks created by Standard & Poor’s. The index is considered to represent the stock market's performance in general. Indexes do not incur fees, and it is not possible to invest directly in an index.