Equities Market Research

2025 brought many wins for the U.S. Exchange Traded Fund (ETF) industry spanning multi-share class approval, a rules-based approach to digital asset ETP development, record flows and record product launches. Product innovation continues to drive the ETF renaissance, culminating best-in-class thinking across mandate structuring, distribution and service provider engagement.

Constituting over 83% of U.S. ETF launches in 2025, active ETFs are redefining measures of success beyond benchmark attribution — instead focusing on how fund mandates are addressing target clients’ risk requirements and performance goals. Active mandates continue to accumulate interest across client segments as allocators choose these ETFs not only for their tailored investment mandates, but as alternatives to other distribution channels such as structured notes and annuities.

In 2025, the ETF space was marked by notable partnerships, as household investment management names combined ETF distribution prowess with institutional sub-advisory capabilities across the year’s biggest ETF launches on the Cboe BZX Exchange. Adding to its list of ETF accolades, JPMorgan Asset Management launched the JPMorgan Active High Yield ETF (JPHY), the industry’s largest active ETF launch ever. Through partnerships with Vanguard and Hartford, Wellington Management came to market in 2025 offering institutional strengths in active management and derivatives. Other notable sub-advisory arrangements in 2025 included derivatives ETF expert Milliman enabling ARK Invest’s debut tranche of buffered ETF products, as well as international specialist Sands Capital sub-advising ETF products manufactured by Touchstone.

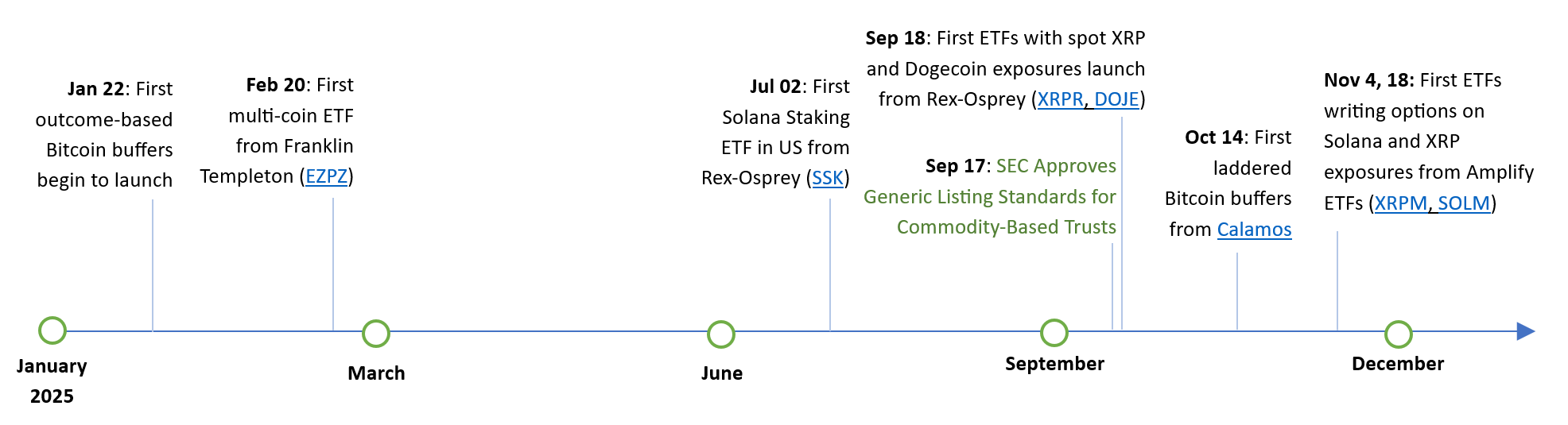

The world of digital assets never stops moving, and crypto ETP development was no exception. Following nearly a decade of advocacy to bring the first spot bitcoin ETPs to market in 2024, masses of new crypto ETP mandates in 2025 ran the gambit of physical “alt-coins”, futures, staking structures, levered, inverse, option-based income, buffers and index-tracking mandates1.

Source: Cboe Internal Data

In September 2025, the Securities and Exchange Commission’s (SEC) Division of Trading and Markets approved exchange proposals to adopt generic listing standards for Commodity Based Trust Shares (CBTS). Under this framework, exchanges may list and trade Commodity-Based Trust Shares that meet the requirements of the approved generic listing standards without first submitting a proposed rule change to the Commission pursuant to Section 19(b) of the Exchange Act.2

Source: Cboe Internal Data

2025 continued the golden age of fixed income3, as unwinding inflation and real rates supported both IG and HY coupons following years of near-zero rates. U.S. fixed income ETF assets under management (AUM) increased more than $450 billion in 2025 despite perpetuated curve steepening expectations driving over $4.5 billion of assets out of 20y+ Treasury bond ETFs. Some longer-dated Treasury assets found their way into option-writing funds like the iShares 20+ Year Treasury Bond BuyWrite Strategy ETF (TLTW), Amplify Bloomberg U.S. Treasury Target High Income ETF (TLTP), NEOS Enhanced Income 20+ Year Treasury Bond ETF (TLTI) and Global X Treasury Bond Enhanced Income ETF (TLTX) — representing a diversity of income-focused alternatives to Treasury coupons.

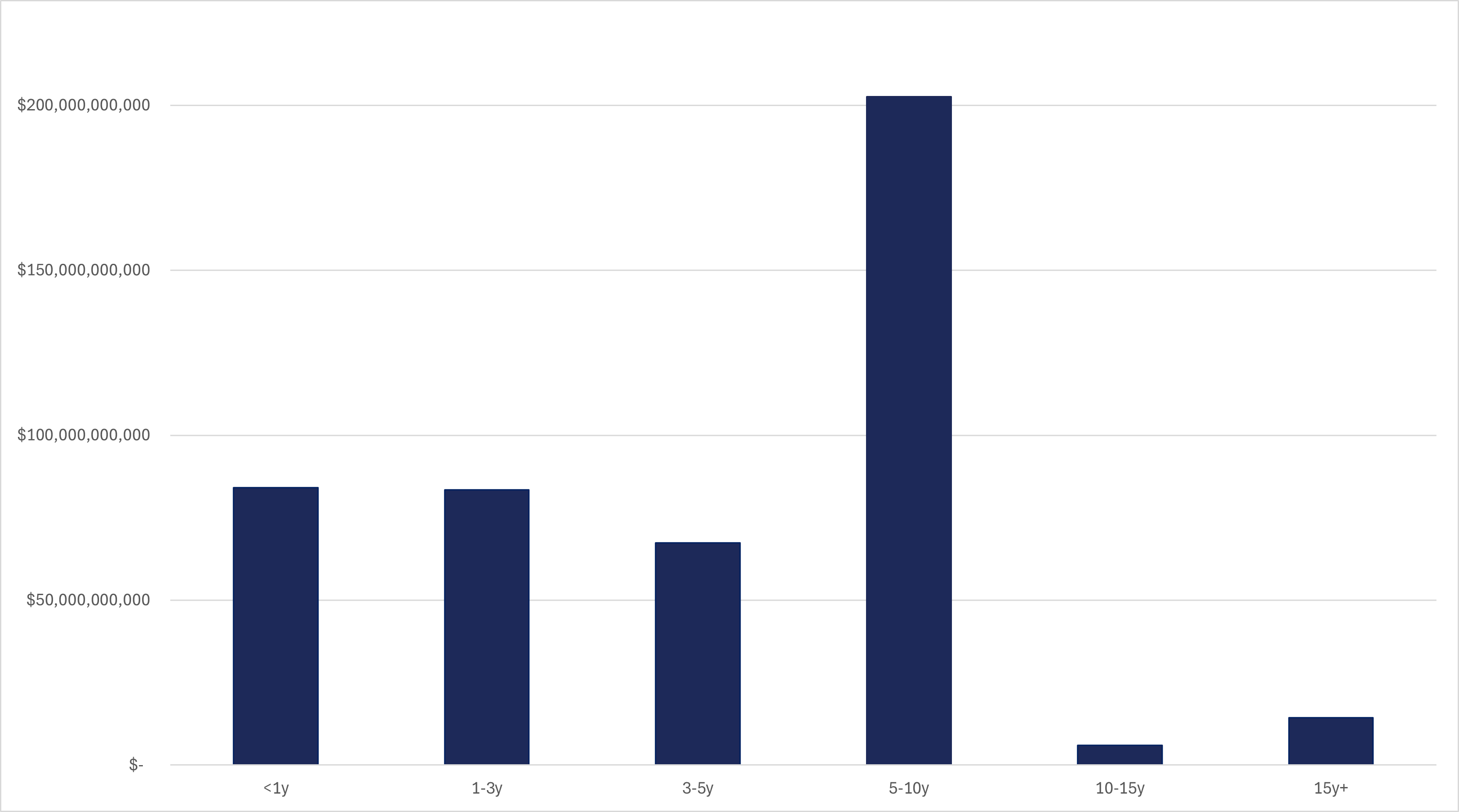

More than 175 new fixed income ETFs launched in 2025, a 25% increase over the amount of fixed income ETF products available in the U.S. market at the end of 2024. Vanguard kept busy throughout the year, increasing its fixed income ETF lineup by over 40%, capturing numerous bond segments across duration baskets under 15 years. PGIM instead focused on corporates, manufacturing three duration baskets — 0-5 year, 5-10 year, and 10+ year — following a similar expansion into municipal ETFs in 2024, and historically diverse coverage of bond mandates.

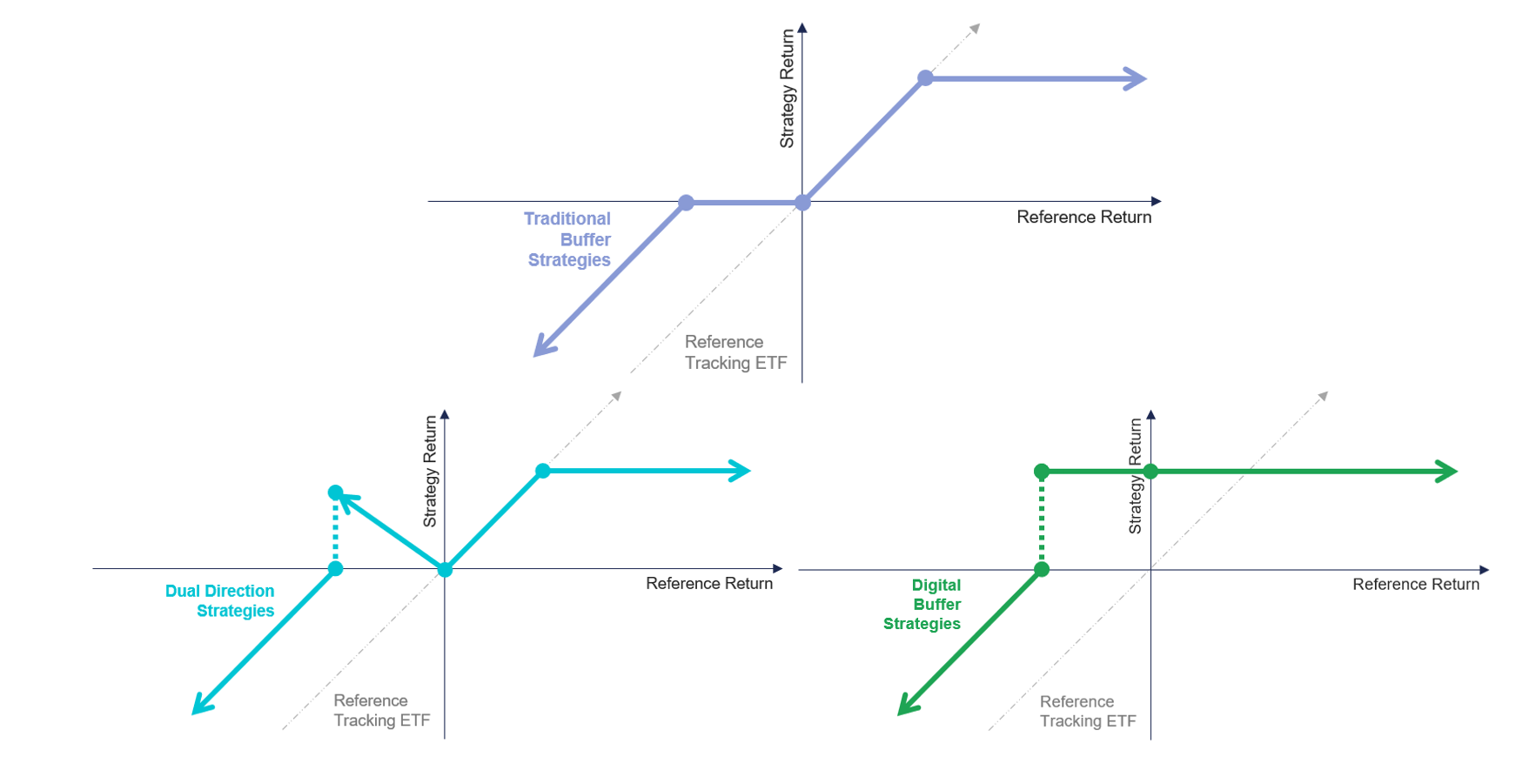

Buffered ETF managers had a busy year characterized by new entrants, new outcomes and even new ways to collateralize options, with option box spreads, in the ETF wrapper. Amidst a choppy quarter for U.S. equities, FT Vest debuted its “Digital Buffer” strategy shortly after manufacturing “Dual Directional” product, introducing yet another variation on traditional buffers to an expansive product lineup.

Source: Cboe Internal Data

ARK Invest, Aptus, and BufferLabs each debuted new ETFs in October as well, bringing a new reference asset and differentiated solutions to the buffer category. ARK Invest started the month with its ARK DIET Q4 Buffer ETF (ARKT) — a tailored buffer strategy referencing the manager’s flagship ARK Innovation ETF (ARKK). Rooted in proprietary research, BufferLABS US Equity Dynamic Buffer ETF (BFLB) aims to optimize upside participation while maintaining downside protection by dynamically rebalancing between traditional buffered ETF baskets. Experienced option-based manager Aptus Capital debuted mid-month, adding a full shelf of quarterly 15% buffers to a lineup of over $5 billion of ETF assets.

Outside outcome-based strategies, Cboe welcomed the JP Morgan Equity and Options Total Return ETF (JOYT), a total return solution combining multi-cap dividend income with an option overlay that aims to enhance income and reduce portfolio volatility. TrueShares’ latest active fund, the TrueShares Convex Protect ETF (PVEX), lays out a scalable, convexity-engineered solution designed to meaningfully capture gains in rising markets while cushioning against significant market decline.

Source: Bloomberg, Cboe Internal Data

Synthetic yield strategies continued to dominate the option-based ETF category in 2025, pitching a diversity of advantages against traditional benchmarks and breathing new life into assets that normally do not return capital. Rather than traditional approaches to building on existing dividend yield or coupon-based yield, these new products look to the existence of an implied volatility market around a reference asset. These fund strategies are focused on financial engineering products’ capital appreciation versus return of capital, accounting for features including, but not limited to, remittance frequency, reference asset class and limits.

The list above points to the sheer variety of income-generating ETFs available today referencing Tesla. In 2025, Tesla was a higher-beta, mega-cap equity, but its common stock does not pay dividends. Yet, a growing handful of ETF managers are meeting investors interested in both the underlying stock and previously absent returns of capital. Tesla income ETFs alone saw 75% new product growth, compared to the number of products available at the end of 2024. Newer product launches reflect more conservative returns of capital as YieldMax debuted on Cboe with the YieldMax TSLA Performance & Distribution Target 25 ETF (TEST), joining likes of REX TSLA Growth & Income ETF (TSII), Roundhill TSLA WeeklyPay ETF (TSLW), and early entrant Kurv Yield Premium Strategy Tesla ETF (TSLP).

Even the most conservative yield mandates continued to gain traction. Alongside the juggernaut $128.5 billion (and growing) 0-3 Month U.S. Treasury Bill ETF category, option-based managers have clinched over $9.5 billion of ETF AUM tracking strategies delivering identical tenors of implied rates priced in the options market as implemented through low-maintenance trades such as box spreads and long (gut) strangles.

Source: Trackinsight, Cboe Internal Data

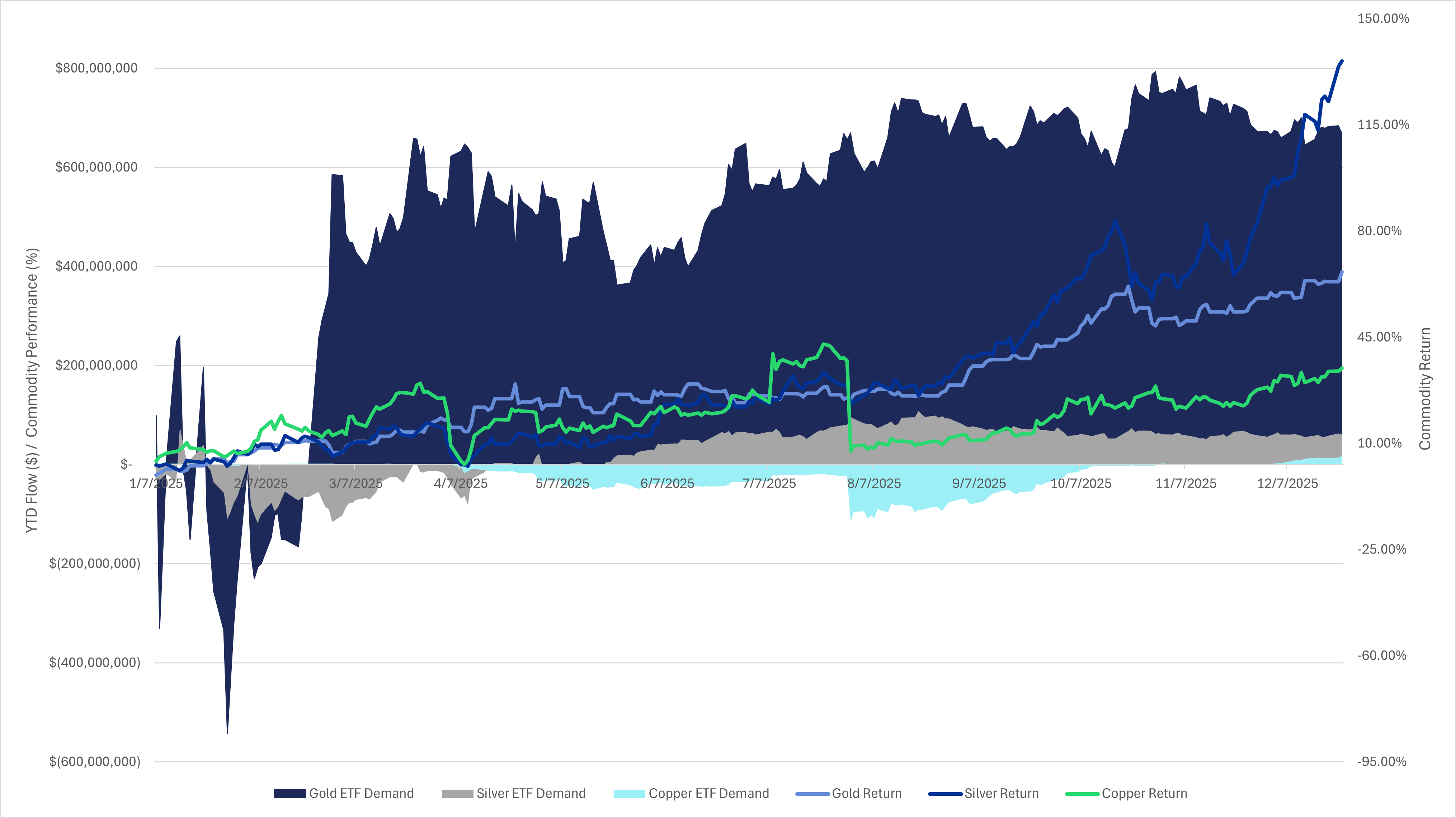

Precious metal ETFs sustained outperformance in 2025 with popular gold and silver miner strategies outperforming respective metals throughout the year. Mining exposure comprises a larger share of silver ETF AUM and flows compared to gold ETFs4, contributing over 35% of net new silver ETF assets over 2025. Despite troy silver outperforming gold in the second half of 20255, resilient flows into gold ETFs were dominated by interest in physical gold ETPs that offset 2025 net outflows from gold miner ETFs. Gold ETFs ultimately led metal ETF category flows, gathering $45.9 billion over 2025 — marking approximately 10 times more accumulated inflow for every point gold appreciated compared to silver ETFs6.

ETF issuers leaned into new gold and silver yield mandates in 2025, wasting little time in staking coverage. NEOS expanded into gold with the NEOS Gold High Income ETF (IAUI) while Roundhill added both Gold and Gold Miner strategies to its popular WeeklyPay shelf. Kurv initiated coverage on both precious metals with the Kurv Gold Enhanced Income ETF (KGLD) and Kurv Silver Enhanced Income ETF (KSLV) — the first option-writing ETF to focus exclusively on physical silver. Copper ETFs weathered a volatile year with 2025 ETF flows edging positive in December, and mining strategies like the Themes Copper Miners ETF (COPA) benefiting from sector tailwinds.

Among 2025’s largest wins for the U.S. ETF industry, the SEC granted exemptive relief to Dimensional Fund Advisors (among others) and also approved exchange rules to list and trade Class ETF Shares. Cboe helped spearhead this initiative in 2024, paving the way for widespread adoption of this important market structure evolution in the U.S.

Beyond Class ETF Shares, Cboe supported the ETF industry throughout 2025 through listing and trading record asset conversions to ETFs from SMAs and mutual funds. During this time, the successful conversion of the iShares High Yield Muni Active ETF (HIMU) ranked among the year’s largest mutual fund transitions. 2025 was the first year where ETFs outnumbered listed companies in the U.S. — a drive-by moment between two secular listing trends and a nod to the rising role of ETF listing exchanges.

We expect more investors and traders to adopt ETFs in 2026, and look forward to ETF advocacy across market structures, distribution channels and regulators. Cboe looks forward to continued operation of our trusted ETF markets, and continued advocacy on behalf of client product development and market structure priorities.

1 The first S&P 500 ETF launched in 1993. 13 years later, the first levered/inverse ETFs from ProShares launched in June 2006, Invesco’s S&P 500 BuyWrite ETF (option based) in December of 2007, and the first S&P 500 buffers launched another 11 years later in 2018.

2 SEC.gov | SEC Approves Generic Listing Standards for Commodity-Based Trust Shares

The information provided is for general education and information purposes only. No statement provided should be construed as a recommendation to buy or sell a security, future, financial instrument, investment fund, or other investment product (collectively, a “financial product”), or to provide investment advice.

3 Active Fixed Income | BlackRock

4 Gold, silver, copper ETFs defined as any spot, futures, geared, option-writing, buffered, or multi-asset fund primarily featuring gold, silver, or copper asset exposure, respectively.

5 Gold, silver copper commodity price represented as price performance of respective ETFs GLD, SLV, CPER from dates Jan 2, 2025 to December 31, 2025

6 ‘accumulation’ of ETF flows defined as dividing net flow over a period of time by change in underlying asset price over that time (e.g. if over a period of time, copper ETFs total $100 billion of creations, $50 billion in redemptions, all while copper price moves up 50%, copper ETFs may be viewed as accumulating $1 billion for every 1% copper commodity appreciated)

In particular, the inclusion of a security or other instrument within an index is not a recommendation to buy, sell, or hold that security or any other instrument, nor should it be considered investment advice.

Past performance of an index or financial product is not indicative of future results.

Brokerage firms may require customers to post higher margins than any minimum margins specified.

Investments in ETPs involve risk, including the possible loss of principal, and are not appropriate for all investors. Non-traditional ETPs, including leveraged and inverse ETPs, pose additional risks and can result in magnified gains or losses in an investment. Specific risks relating to investment in an ETP are outlined in the fund prospectus and may include concentration risk, correlation risk, counterparty risk, credit risk, market risk, interest rate risk, volatility risk, tracking error risk, among others. Investors should consult with their tax advisors to determine how the profit and loss on any particular investment strategy will be taxed.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/global-disclaimers/.