While the SPX® Index is up over 9% over the past month, the rally has been incredibly concentrated, led largely by the Tech sector (up 20%). In fact, 4 of the 11 S&P sectors are down over the past month and another 3 are mostly unch’d. In other words, we’ve seen incredibly high dispersion underneath the index surface, which helps explain why index volatility is so muted while single stock volatility remains elevated (e.g. VIX® Index down 4 pts vs. VIXEQSM Index up 1 pt over the past month). The difference between the two has widened to the 98th percentile high.

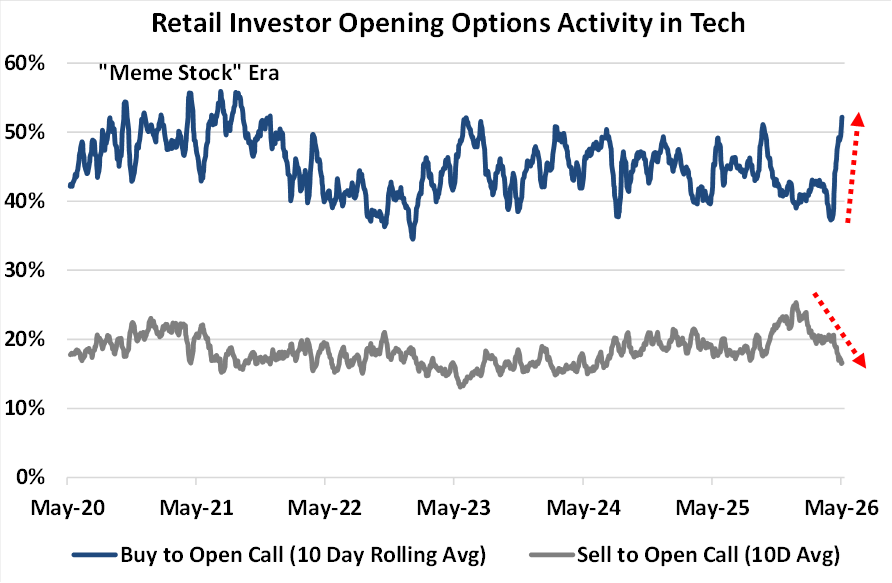

We’ve seen a sharp uptick in call buying activity from retail investors on our exchanges, with over 52% of all retail opening activity in 10 mega-cap Tech stocks (Mag-7 plus AMD, PLTR, and AVGO, which collectively make up the Cboe Magnificent 10SM Index, or MGTN Index) consisting of call buying. As seen in the chart below, that is up over 15 ppts from last month and is the highest since the covid “meme stock” era.

This is a reversal of the trend we saw earlier this year where retail investors were getting more defensive in Tech stocks with outright call buying activity dropping, put buying increasing, and call selling/overwriting activity jumping to multi-year highs. With the sharpness of the recent Tech rally, overwriters have pulled back, with the share of retail opening activity that is selling calls dropping from 24% to now 17%.

Chart: Retail Call Buying in Tech Nears 2021 Extremes