Despite gold’s reputation as an inflation hedge, its track record has been rather poor in recent years. In 2022, gold fell over 20% from the highs as inflation surprised to the upside. It’s down over 15% this month as stagflation risks have reemerged on the back of the Iran war, with the market now pricing in ~30% probability of a rate hike by year-end (vs. pricing in 2.5 cuts a month ago). Positioning in gold options has also shifted, with demand for puts increasing. After being persistently inverted over the past year (i.e. calls trading at a premium to puts), GLD skew has steepened to a 1-year high, with puts now trading at a premium to calls.

The unreliability of traditional safe havens (e.g. bonds and gold) in recent years is a key driver behind the rise of options-based ETFs, particularly buffer ETFs, as investors turn to options for portfolio protection (for more, see our “Beyond 60/40” paper). FLEX options, which are used in buffer ETFs to give the defined outcome, have grown in popularity, with a record 4.1M contracts trading on Friday (5% of total market volume).

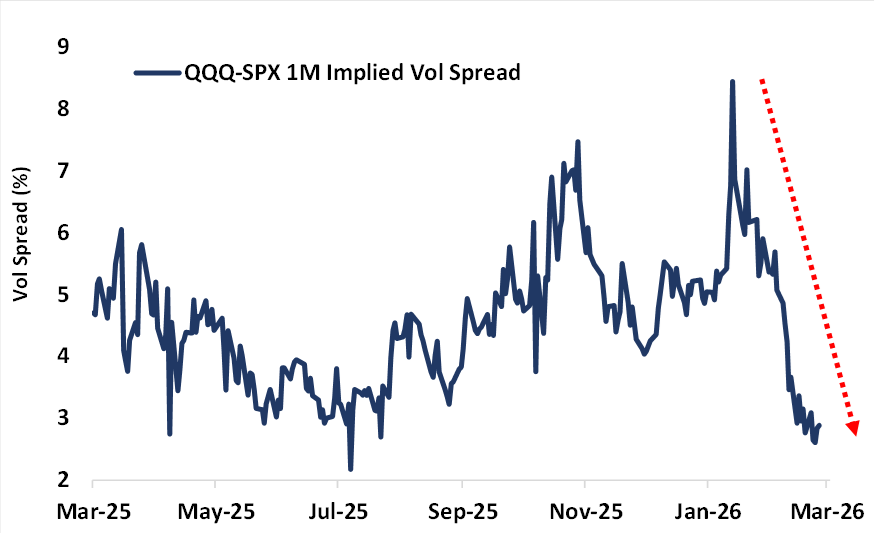

Compared to a month ago, average single stock vol (as measured by the VIXEQSM Index) is roughly unchanged at 40.8% while the VIX® Index is ~8 pts higher on the back of higher stock correlation, with the COR1M Index up over 25 pts during that time. As focus shifts away from AI to macro risk, the excess risk premium for Tech stocks have dissipated. This can be seen in the QQQ-SPX 1M implied volatility spread which has narrowed from a 1-year high of 8.4% in Feb to near a 1-year low of 2.6% currently. See chart below.