Data Analytics and Indices

The first couple months of 2026 have been marked by continued geopolitical risks and renewed discussion of tariffs, impacting U.S. and global markets. U.S. equity indices, including the Russell 2000 Index (RUT), experienced their first daily loss greater than 1% of 2026 immediately following Martin Luther King Day. Market volatility further increased with the Cboe Russell 2000 Volatility Index (RVX) reaching a year-to-date high at the beginning of March, driven by renewed geopolitical tensions in the Middle East that drove oil prices higher and adding further headwinds for equities. With the return of these volatile market conditions, volatility reduction strategies, such as covered calls, are once again in high demand to help investors navigate the heightened market volatility.

The current environment underscores the need for two new Cboe indices, the Cboe Validus Russell 2000 Dynamic Call BuyWrite Index (CALRD) and Cboe Validus Russell 2000 Dynamic PutWrite Index (RUTD). These are the latest addition to Cboe’s dynamic series, joining the Cboe Validus S&P 500 Dynamic Call BuyWrite Index (CALD) and Cboe Validus S&P 500 Dynamic PutWrite Index (PUTD).

CALRD is a rules-based strategy that overlays short call positions on a fully invested S&P 500 Total Return portfolio. Unlike traditional monthly BuyWrite strategies that sell calls once per month, CALRD uses a dynamic, five-day rolling structure, selling RUT 1-month call options on each of the five business days leading up to standard expiration.

In contrast, PUTD tracks the value of a rule-based investment strategy which consists of overlaying a basket of RUT standard-expiry short put options over a money market account invested at the 4-week daily Treasury Bill rate.

The strikes are a function of the front month 25-delta call implied volatility. In low-volatility environments, CALRD sells calls (and RUTD sells puts) closer to at-the-money strikes. Conversely, as volatility rises the calls in CALRD are sold further out-of-the-money while the puts in RUTD are sold deeper in-the-money. Since both indices reference the 25-delta call implied volatility, this structure allows the strategies to dynamically adjust based on current market conditions. This increases the potential to retain options premiums, especially after market pullbacks. On each roll date, only one-fifth of the total notional options exposure is turned over, which helps reduce timing risk and smooth the path of returns.

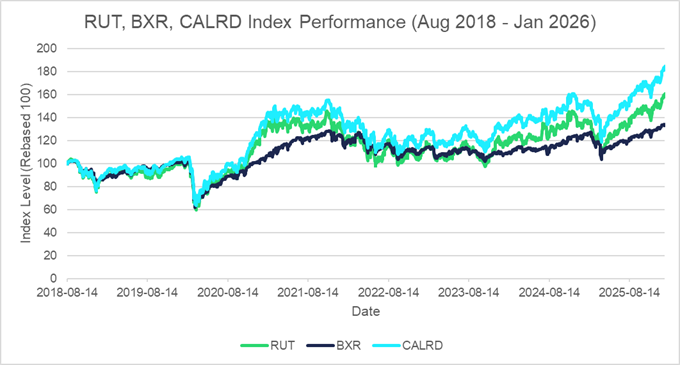

The performance chart below provides a direct comparison between three key indices: the benchmark Russell 2000 Index (RUT), the Cboe Russell 2000 BuyWrite Index (BXR) and the Cboe Validus Russell 2000 Dynamic Call BuyWrite Index (CALRD). The BXR represents a traditional BuyWrite strategy on RUT, in which call options are systematically written at-the-money once per month. In contrast, CALRD employs a dynamic approach, as previously outlined, which involves a five-day rolling structure for selling call options.

This comparative analysis demonstrates that CALRD consistently outperforms both the traditional at-the-money BuyWrite index (BXR) and the benchmark RUT. The dynamic nature of CALRD allows it to adapt more effectively to changing market conditions, contributing to enhanced returns relative to the more static approach of BXR and the underlying index.

Source: Cboe

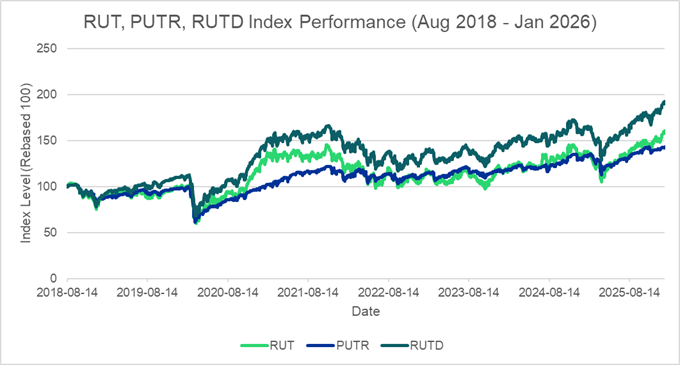

Similarly, the chart below compares the benchmark RUT, Cboe Russell 2000 PutWrite Index (PUTR) and PUTD. The dynamic PutWrite PUTD also outperforms the traditional at-the-money PutWrite PUTR and the benchmark RUT.

Source: Cboe

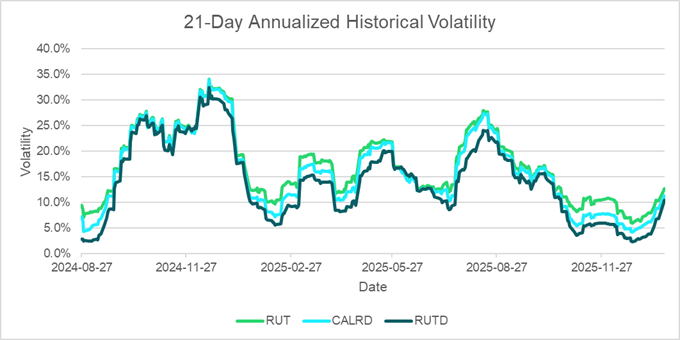

The following chart compares the 21-day annualized historical volatility between RUT, CALRD and RUTD between August 2024 and January 2026. Like other BuyWrite and PutWrite indices, CALRD and RUTD are less volatile compared to the benchmark.

Source: Cboe

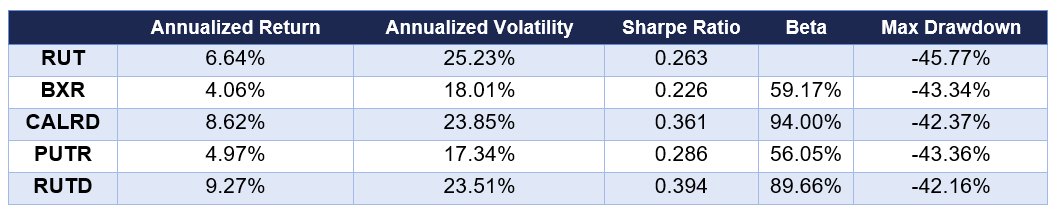

When comparing RUT, BXR, PUTR, CALRD and RUTD, the annualized returns indicate that CALRD and RUTD have the potential to outperform their benchmark when strike prices are dynamically selected according to implied volatility levels, which may facilitate greater capital growth.

The following performance metrics show a comparison between the benchmark RUT and both the traditional BuyWrite and PutWrite indices (BXR and PUTR), as well as the dynamic BuyWrite and PutWrite indices (CALRD and RUTD), for the period from August 2018 to January 2026.

Both CALRD and RUTD exhibit lower volatility as some of the upside volatility inherent in the underlying benchmark is reduced. However, this reduction is less pronounced than in their respective traditional BuyWrite and PutWrite (BXR and PUTR) indices, since those utilize at-the-money strikes which neutralize more of the upside volatility.

Evaluating return in conjunction with volatility, CALRD and RUTD achieve superior Sharpe ratios compared to the traditional BuyWrite and PutWrite indices and RUT. Furthermore, CALRD and RUTD also demonstrate better results when looking at maximum drawdown.

In summary, CALRD and RUTD have so far demonstrated effective volatility dampening properties while keeping pace with RUT during recovery periods. The layered and rules-based options writing approach of these dynamic indices offers a differentiating risk-return profile, making them particularly well-suited for sideways or uncertain markets where traditional equity exposure may underperform.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/global-_disclaimers/. These products are complex and are suitable only for sophisticated market participants. In certain jurisdictions, Cboe Company products are only permitted for investment professionals, certified sophisticated investors, or high net worth corporations and associations. These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position. Market participants should put at risk only funds that they can afford to lose without affecting their lifestyle. © 2026 Cboe Exchange, Inc. All Rights Reserved.