Implied volatilities fell across asset classes last week on softer than expected CPI and easing trade tensions. Equity volatility led the way, with the VIX® index down 4.4 pts wk/wk to 16.4%, falling to the 39th percentile low over the past year. Gold implied volatility moderated, even as realized volatility surged higher, driving the 1M implied-realized vol spread from a high of +9% to now -12%. Notably, investors used the sell-off to add to upside calls, with GLD skew becoming even more inverted over the past week.

Rates vol declined last week on the back of the soft inflation data, with both MOVE and VIXTLT index falling to a 1-year low ahead of this week’s FOMC meeting where the Fed is widely expected to cut rates by another 25bps (99% implied probability in the OIS market). Very little volatility is priced into the equity market as a result, with SPX® weekly options implying just a 1.0% move for Wednesday – a typical one-day move with the VIX index at 16%.

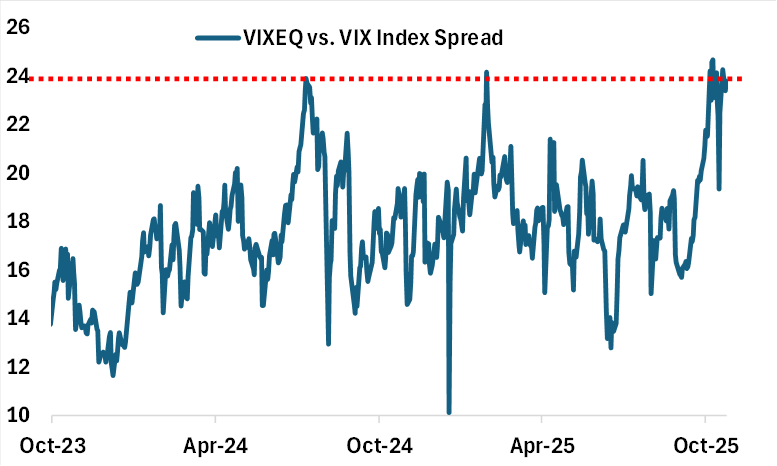

The spread between single stock vol vs. index vol, as measured by the VIXEQSM vs. VIX index spread, widened back to near all-time high of 24% last week (see chart below), ahead of key tech earnings (5 of the Mag-7 companies reporting this week).

Chart: Single Stock Vol Trading at Near Record Premium vs. Index Vol