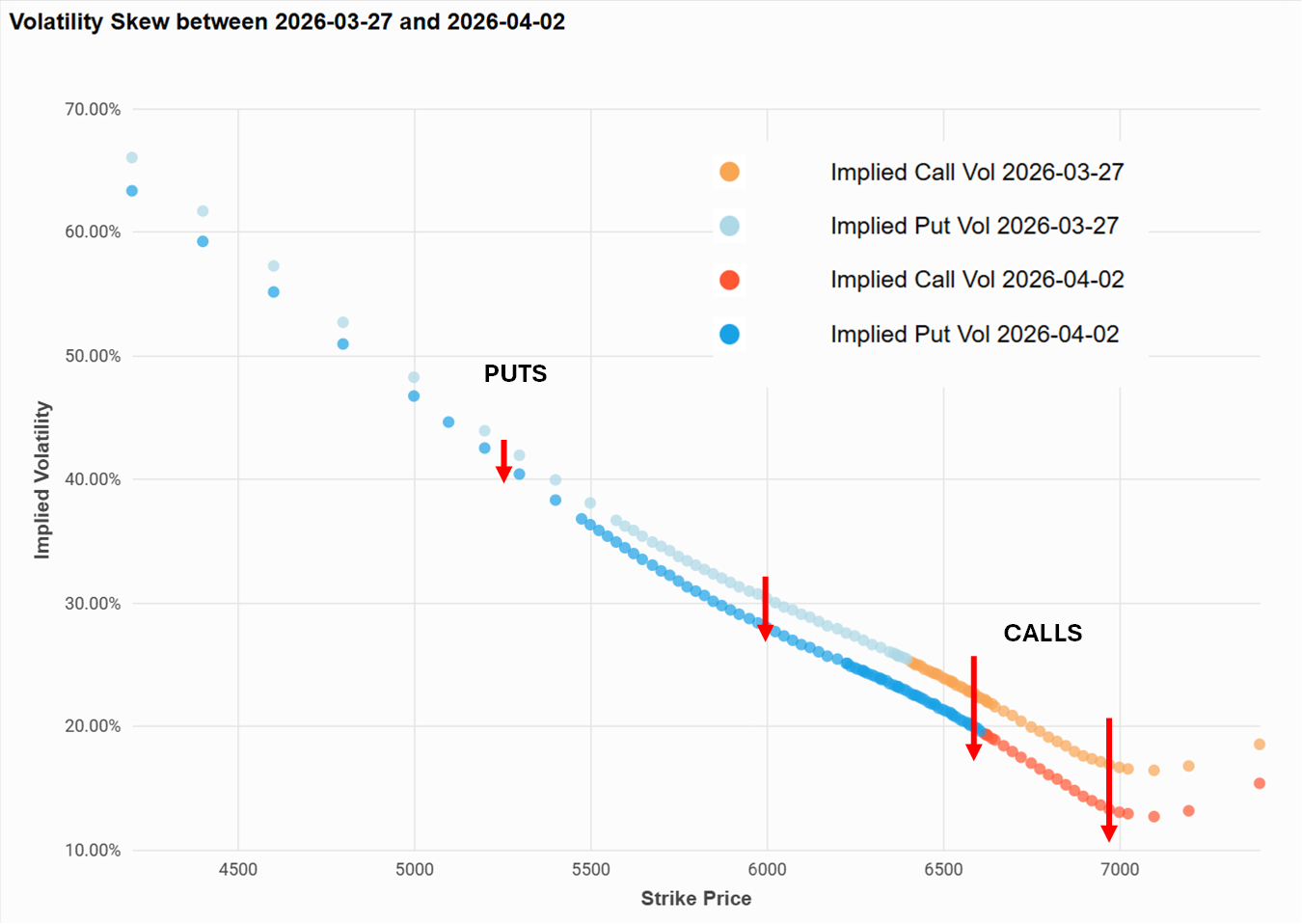

Options traders have been using SPX® options to fade big moves in the market – in both directions. Last week we highlighted how investors have been selling out of hedges on pullbacks and switching into upside calls to play for a rebound. On the rally last week, we saw the opposite – demand for hedges picked up while calls were aggressively monetized. The decline in SPX call skew and call convexity (see chart below) contributed over 2 pts to the 7 pt decline in the VIX® Index last week.

SPX 1M put skew steepened off the lows on the back of stronger hedging demand, rising from the 2nd percentile low to the 37th percentile currently. Most of the hedging flow has been tactical in nature (e.g. concentrated in the shorter-dated tenors) while longer-dated portfolio hedging demand still remains muted. SPX 6M skew, for example, is in the 10th percentile low.

Despite the risk-on tone in the market last week, oil prices continued their upward climb, with WTI crude ending the week over $111/bbl. There’s been very little change in the positioning in the oil options market despite talks of a ceasefire, with demand for calls still outpacing puts and oil skew remaining extremely inverted across the front 6-month tenors.

Chart: Options Traders Fading the Rally Through Selling Calls