Global Markets

Tradable Products

Featured Products

The first quarter of 2026 saw record trading volumes in European equities, driven by sustained investor interest in the region alongside ongoing geopolitical developments. For Cboe Europe, it was a record-breaking period, as we retained our position as Europe’s largest equities exchange and delivered all-time high trading days across some key services.

1. Record Growth Across European Equities Markets

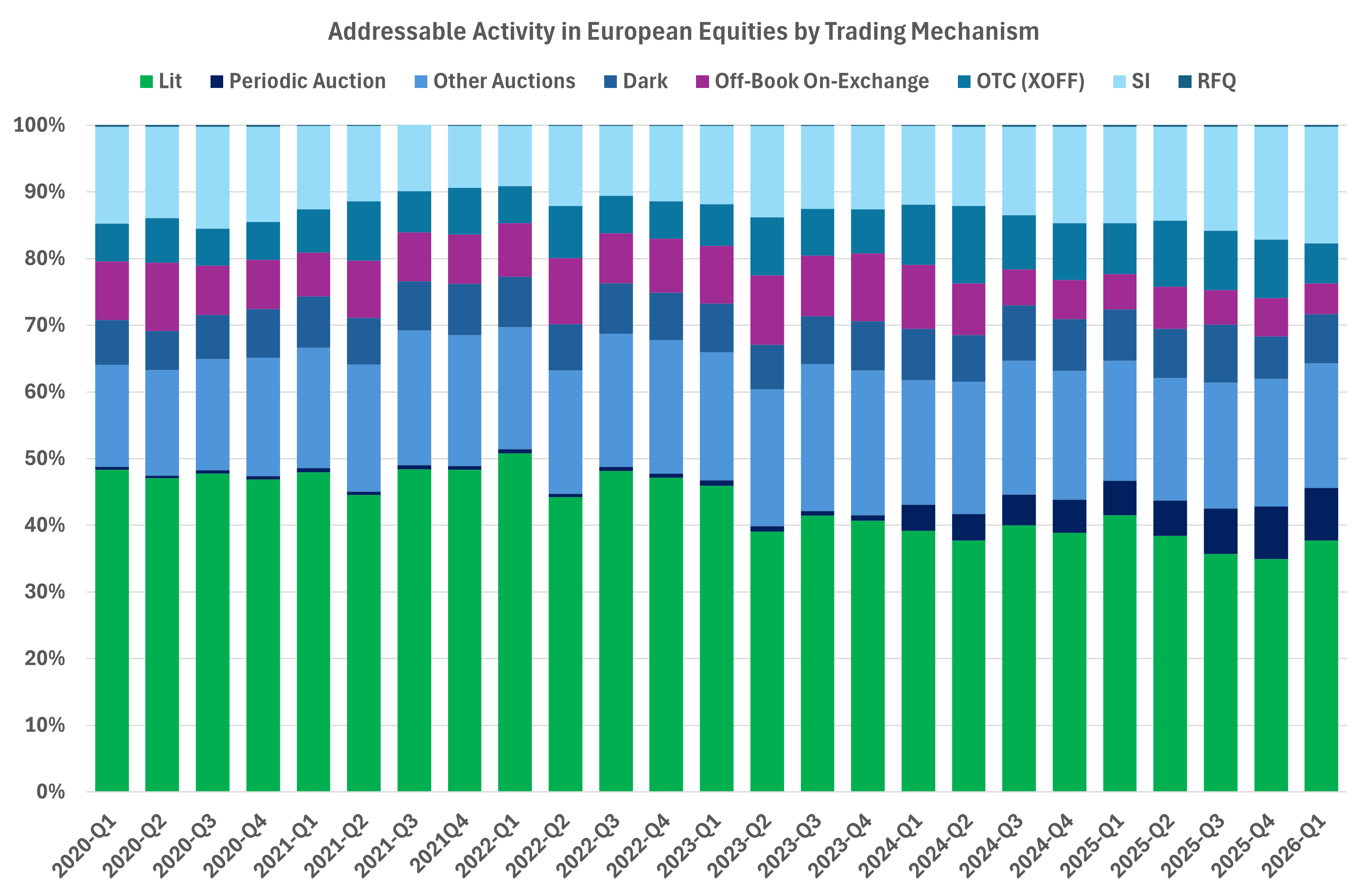

Across the industry, European equities volumes reached an all‑time high in Q1, with total addressable average daily value-traded (ADVT) increasing 23% year‑over‑year to €94.4bn. This growth was accompanied by a slight increase in activity on lit continuous order books, as investors prioritised execution speed and certainty amid heightened market volatility. Over the longer term, the trend remains one of declining lit continuous market share and increased adoption of alternative trading mechanisms, including Periodic Auctions and Systematic Internalisers (SIs).

2. Cboe Europe Delivers Strong Performance Across Mix of trading services

Cboe Europe remained Europe’s largest equities exchange throughout the quarter, with an average market share of 25.5% - our highest level since Q4 2011. The quarter also set a new record for ADVT at €17.3bn, while March established a new monthly high of €18.6bn. Five of the ten highest trading days in Cboe Europe’s history occurred during the quarter, with records across key services such as Periodic Auctions, Cboe Closing Cross (3C) and Cboe BIDS VWAP-X.

3. Continued Progress in Retail Trading

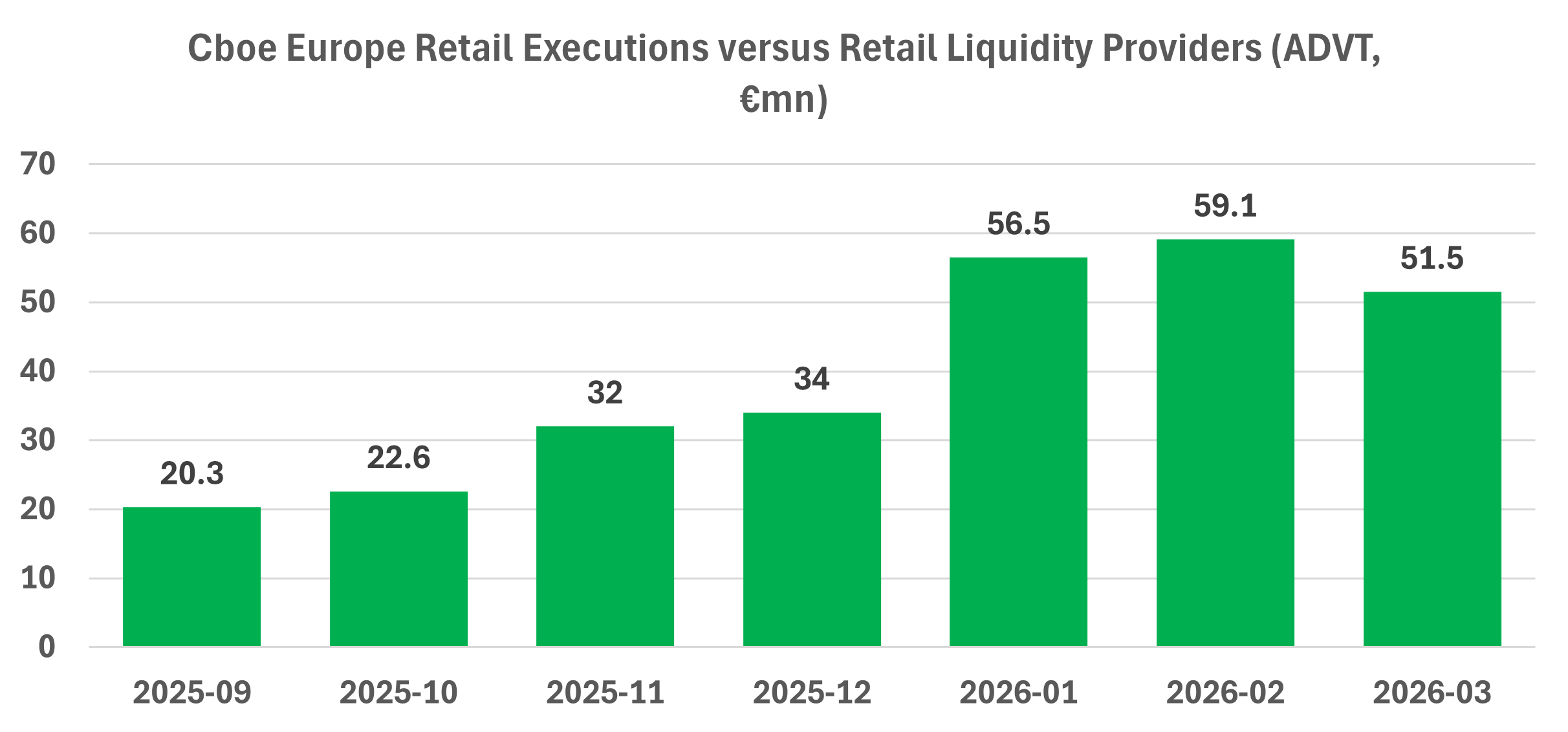

We continued to build momentum with our pan-European EBBO Retail Service, which provides retail brokers with free execution in over 9,000 stocks and ETFs across Europe, including the ability to execute at or better than the European Best Bid and Offer (EBBO). Participation has increased steadily, with total execution value against retail liquidity providers exceeding €5.7bn since launch by the end of Q1 - and a record daily volume of €91.7m on 3 March.

4. Key Priorities for the EU’s Capital Markets Integration Reforms

Cboe recently published a whitepaper setting out our key priorities for the EU’s Market Integration and Supervision Package (MISP), which is vital to supporting the development of more integrated and globally attractive European capital markets. Our recommendations focus on mandating clearing interoperability for large cash equity exchanges, preserving choice and competition for institutional trading activity and creating a genuinely pan‑European market for retail investors.

5. Market Data Price Changes

Cboe has also published updated market data fees in line with the EU’s new Reasonable Commercial Basis (RCB) requirements, which take effect in August. The revised fee structure is expected to be revenue‑neutral while simplifying licensing arrangements for users. For more details, see the technical notice.

Across the industry, European equities volumes reached an all‑time high in Q1, with total addressable average daily value traded (ADVT) increasing 23% year‑over‑year to €94.4bn.

This growth was accompanied by increased activity on lit continuous order books quarter-over-quarter, as investors prioritised execution speed and certainty amid heightened market volatility. Lit continuous order books accounted for 37.7% of all activity in Q1, up from 34.9% in Q4 2025. Over the longer term, however, the trend remains one of declining lit continuous market share and increased adoption of alternative trading mechanisms, including Periodic Auctions and Systematic Internalisers, which accounted for 7.9% and 17.5% of activity in Q1 2026 respectively, compared with 5.2% and 14.5% a year ago.

These mechanisms are now well-established parts of the European market ecosystem because of the distinct value they deliver to end investors, and their growth reflects evolving investor needs and more sophisticated execution strategies. Cboe Europe’s mix of trading services, including being the largest Periodic Auction operator, drove our growth. We retained our position as Europe’s largest equities exchange throughout the quarter, with an average market share of 25.5% - our highest level since Q4 2011. The quarter also set a new record for ADVT at €17.3bn, while March established a new monthly high of €18.6bn. Five of the ten highest trading days in Cboe Europe’s history occurred during the quarter.

Other highlights included:

We continued to build momentum with our pan-European EBBO Retail Service, which provides retail brokers with free execution in more than 9,000 stocks and ETFs across Europe, including the option to execute at or better than the European Best Bid and Offer (EBBO). The service is supported by a dedicated retail liquidity provider programme, which incentivises liquidity providers to display EBBO-level quotes exclusively for interaction with retail flow. Retail orders are also eligible for free execution on other services, including dark trading and periodic auctions, offering additional opportunities for price improvement.

By quarter-end, 12 retail brokers had signed our retail attestation form, supported by six retail liquidity providers, with more than one million trades, across close to 3,400 symbols in 15 European markets. Total execution value against retail liquidity providers surpassed €5.7bn since launch by the end of Q1, with the service reaching a record daily volume of €91.7m on 3 March.

In early March, we enhanced the service through technical changes that enable retail liquidity providers to quote tighter prices for retail orders, improving execution quality and the overall retail trading experience. For further information, please speak with your account manager or refer to the related technical notice.

In other product developments, we continued to explore opportunities to extend our trajectory crossing service, Cboe BIDS VWAP-X, to the EU. As market participants increasingly integrate Periodic Auctions into a broader range of routing strategies, we also have several future releases planned to encourage greater interaction across the spread and further improve execution outcomes. In addition, we plan to expand symbol coverage with additional European growth securities later this year.

Discussions and negotiations continued around the EU’s Market Integration and Supervision Package (MISP), which is now expected to encompass a broader review of market structure issues than originally envisaged. Against a backdrop of growing investor interest in European equities and an evolving market structure, the package presents a timely opportunity to update and refine the regulatory framework established under MiFID - building on its successes while addressing areas where targeted reforms are required to lay the foundations for a more open, integrated and globally competitive European market.

We support the EU’s ambition to create stronger, more integrated and efficient capital markets, but believe greater ambition is needed in several key areas. Our policy recommendations include:

For more details, read our MISP policy whitepaper.

In related developments, we also responded to the UK consultation on the framework for a consolidated tape, reiterating the importance of a revenue-sharing model that appropriately compensates price-forming venues for contributing data to the tape.

The updated Reasonable Commercial Basis (RCB) framework will come into effect on August 23, and governs how trading venues and APA can charge for market data by requiring fees to reflect the cost of producing the data plus a reasonable margin. While Cboe Europe has always followed these principles with its market data fees, the new rules provide clearer guidance on allowable costs, margin levels and how client categories should be structured.

To align with the framework and simplify licensing, Cboe Europe has introduced new client categories based on how customers use the data, removing the need for clients to hold multiple licences and simplifying administrative processes. Cboe Europe expects its new structure to be revenue neutral in Europe and reduce administrative complexity while using terms and concepts consistent with the RCB framework.

For more details, see the technical notice.