Implied volatilities increased across asset classes last week amidst the geopolitical overhang created by the instability of commercial transit along the Strait of Hormuz and mixed signals from Iranian hard-liners undermining the country’s appetite for a resumption of peace talks. Equity, rates, credit, and FX implied volatilities all posted modest gains (see Exhibit 1), with the VIX® Index ending the week 1.25 pts higher to 18.7% - despite the fact that the S&P-500® has rallied to record highs for a YTD return of +4.7%.

Our VIX decomposition analysis (Exhibit 2) showed that the “spot up, vol up” dynamic was driven by a combination of higher fixed strike vols and long risk reversal positioning (i.e., investors selling upside calls to fund downside protection). This positioning has steepened skew from 7th percentile lows last week to 60th percentile levels.

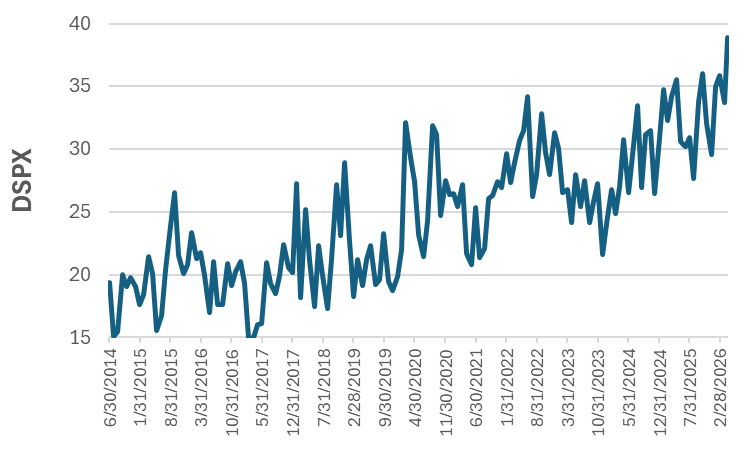

Strong Q1 earnings and ongoing enthusiasm around AI catalyzed by the INTC-TSLA semiconductor/ cloud-infrastructure partnership has pushed stock dispersion towards record highs. (Exhibit 3). As a result, stock implied correlations have fallen sharply since the beginning of the war, with COR1M plummeting from 42% in March to 11% today. See chart below.

Chart: Stock Dispersion Rises to Highs on A.I.-Optimism