Implied volatilities declined across the board last week as the solidification of a US-Iranian peace agreement and the re-opening of the Strait of Hormuz dissipated geopolitical risk premia across the major asset classes. With oil prices falling to a 3-month low (though still at a 20% premium vs pre-War levels), risk sentiment and positioning in the oil markets have both normalized to pre-War levels with 1M oil volatility (OVX) falling 5pts to 54% (65th percentile) and 1M USO call implied volatilities trading just slightly above parity vs comparable maturity put implied vols.

Although the SPX® Index advanced by a modest 0.7% last week, the VIX® Index declined far greater than expected (+4 pts to 17.7) due in large part to the unwind of protective near-the-money hedges and downside convexity positions and repositioned into more bullish synthetic long positions.

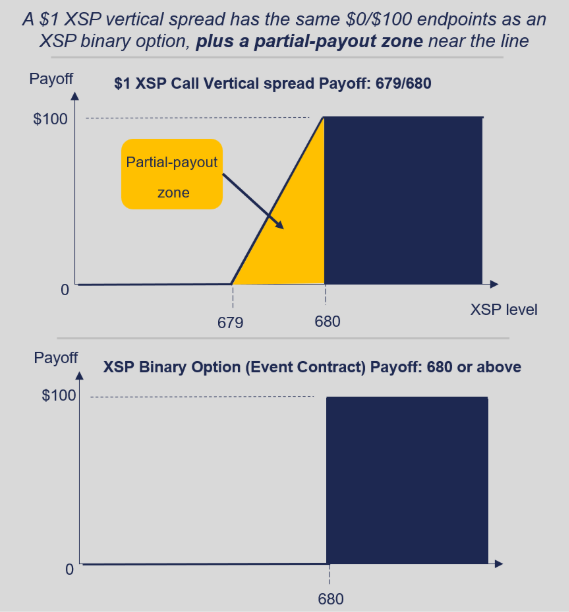

On Monday, June 15, Cboe will add two XSP®-based products to offer simple defined-outcome exposures: XSP Binary Options and Quoted $1 XSP Vertical Spreads. The payoff for XSP Binary Options depends solely on whether the option finishes in or out of the money at expiration. Binary options that finish in-the-money receive the full payout of $100 per contract, while binary options that finish out of the money expire with no payout. By contrast, Quoted $1 XSP Vertical Spreads have the same $0 to $100 payout range, but include an additional partial-payout zone within the $1 interval between the two strikes. As a result, a Quoted $1 XSP Vertical Spread can still have value at expiration when XSP settles within the $1 range between the two strikes, rather than being strictly all-or-nothing. For more information, please visit XSP Binary Options & Quoted XSP Vertical Spreads | Cboe or contact your Cboe sales representative.

Chart: Payoff: Quoted $1 XSP Vertical Spread vs Binary Option