Global Markets

Tradable Products

Featured Products

Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

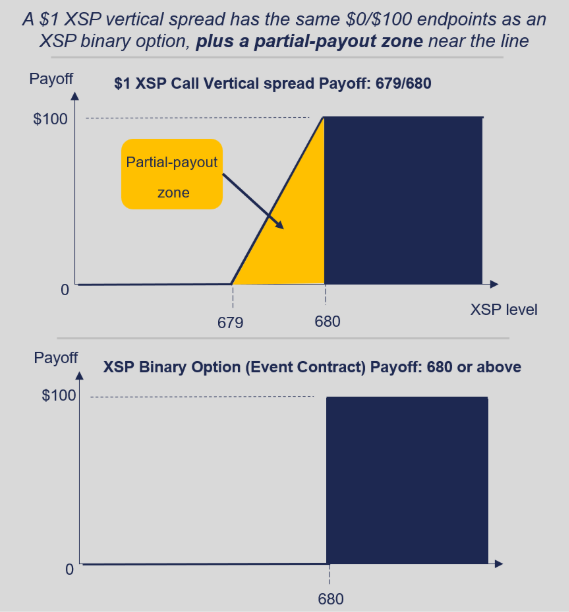

Chart: Payoff: XSP Vertical Spread vs Binary Option

Source: Cboe

*The payoff for XSP Binary Options depends solely on whether the option finishes in or out of the money at expiration. Binary options that finish in-the-money receive the full payout of $100 per contract, while binary options that finish out of the money expire with no payout. By contrast, Quoted $1 XSP Vertical Spreads have the same $0 to $100 payout range, but include an additional partial-payout zone within the $1 interval between the two strikes. As a result, a Quoted $1 XSP Vertical Spread can still have value at expiration when XSP settles within the $1 range between the two strikes, rather than being strictly all-or-nothing. For more information, please visit XSP Binary Options & Quoted XSP Vertical Spreads | Cboe or contact your Cboe sales representative.