Data Analytics and Indices

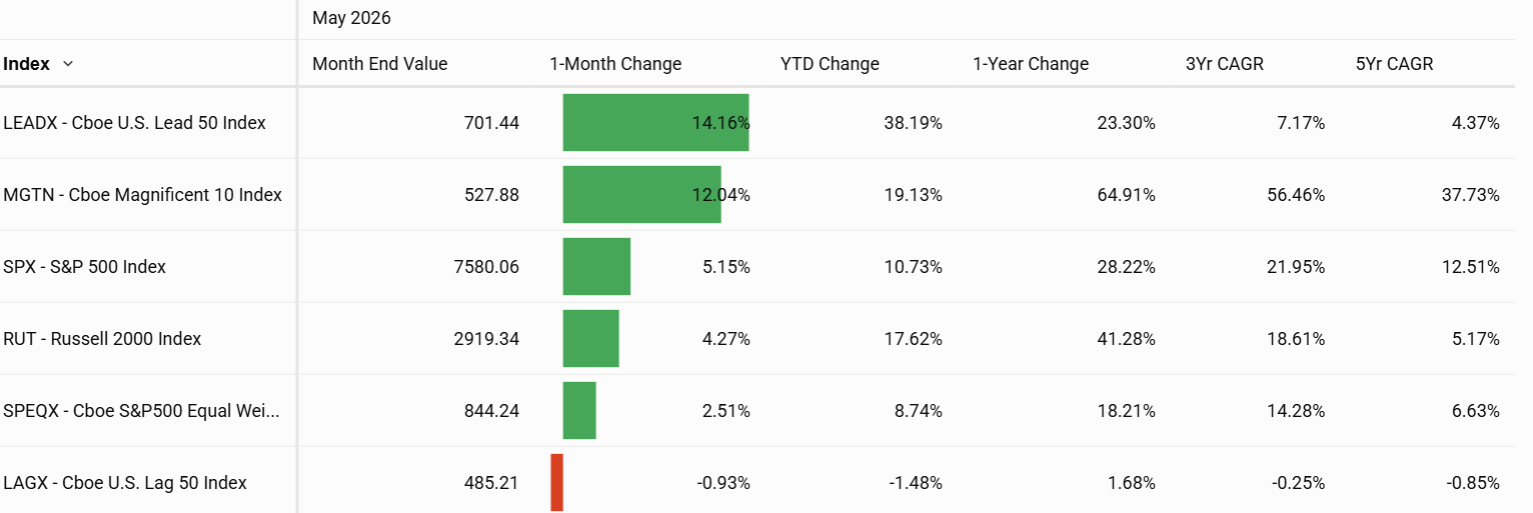

In May, U.S. equities extended April’s strong rebound, with broad indices advancing to new highs amid continued leadership from large-cap technology stocks. The S&P 500® Index gained more than 5% on the month, while the Russell 2000® Index followed closely with a 4.3% increase, leaving year-to-date returns at approximately 10.7% and 17.6%, respectively.

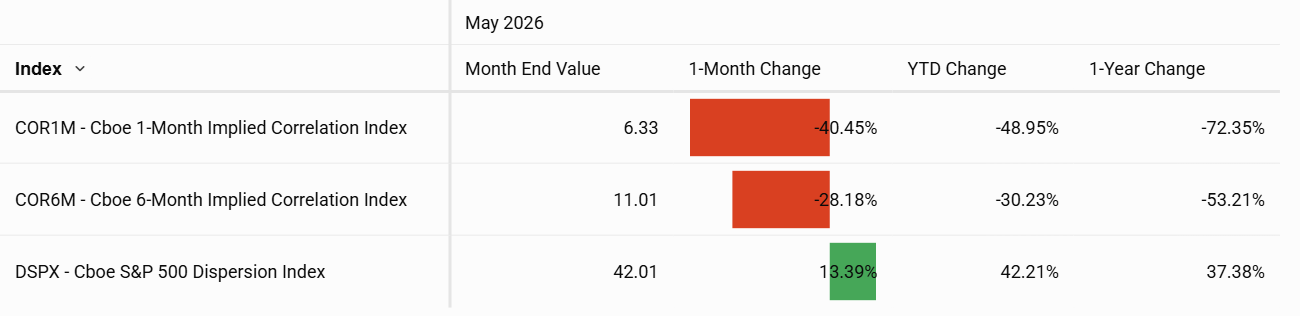

Mega-cap leadership remained a dominant theme. The Cboe Magnificent 10SM Index (MGTN) rose nearly 12% to close at an all-time high of $527.88, representing a gain of almost 39% from the late-March lows. At the same time, measures of dispersion and correlation pointed to a shift in market dynamics. The Cboe 1-Month Implied Correlation Index (COR1M) declined nearly four points, while the Cboe S&P 500 Dispersion Index (VIXEQ) increased roughly four points, signaling expectations for greater stock-specific differentiation rather than broad, macro-driven moves.

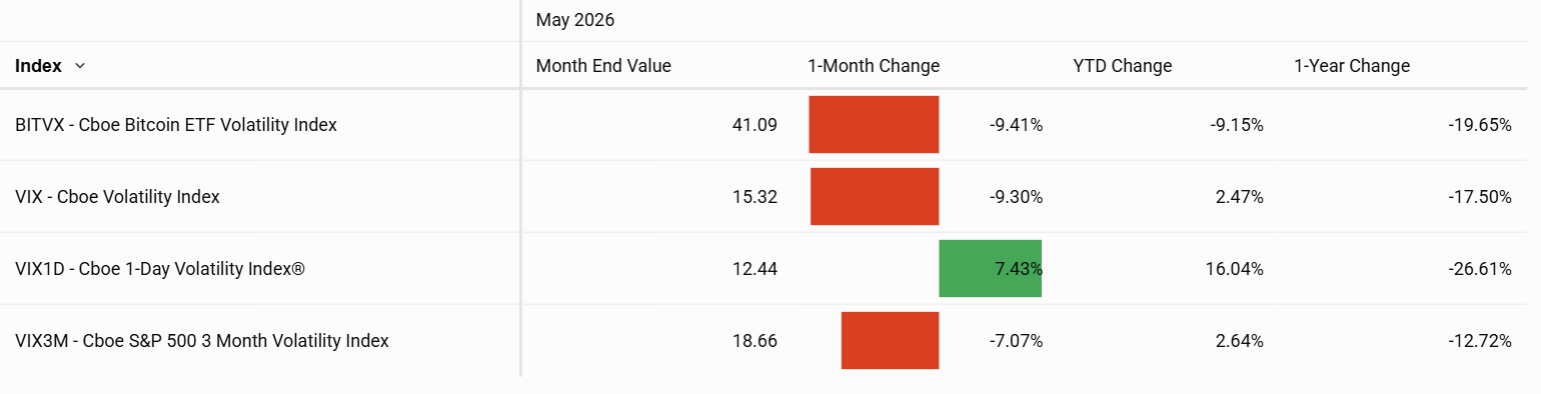

This environment of elevated dispersion coincided with a modest decline in overall volatility. The Cboe Volatility Index (VIX® Index) fell more than 1.5 points to finish the month at 15.32, among the lowest levels observed year-to-date.

Crypto markets diverged from equities. After tracking the broader rally in April, momentum in digital assets softened, with the Cboe Bitcoin U.S. ETF Index (CBTX) declining nearly 4% in May. Volatility in the space remained contained, as the Cboe Bitcoin Volatility Index (BITVX) fell by approximately four points.

Options-based income strategies delivered positive results, supported by the combination of higher underlying prices and subdued volatility. Performance was particularly strong within the Russell 2000 complex, where realized volatility ran consistently below implied levels. The Cboe Russell 2000 Daily Covered Call Index (RTYDCC) led with a gain of 4.65%, while the Cboe Russell 2000 PutWrite Index (PUTR) increased 3.8%.

Source: Cboe Global Markets

The Cboe S&P 500 Index option contract, known by its symbol SPX, is designed to track the underlying S&P 500 Index and help investors achieve broad market protection. SPX® options offer the potential opportunity to manage large-cap U.S. equity exposure and execute risk management, hedging, asset allocation, and income generation strategies. The Cboe S&P 500 Equal Weighted Index option contract, SPEQX, is the equal-weight version of the widely used S&P 500 divided by 10.0. The index includes the same constituents as the capitalization weighted S&P 500, but each company in the S&P 500 Equal Weight Index is allocated a fixed weight - or 0.2% of the index total at each quarterly rebalance. The Russell 2000® Index (RUT) measures the performance of small-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 2000 securities based on a combination of their market cap and current index membership. RUT options are valuable tools for increasing yields and managing risk. The Cboe Magnificent 10SM Index (MGTN) is an equal-weighted equity index designed to measure the price return of a select group of large-cap U.S. technology and growth-oriented companies with listed options. The Cboe U.S. Lead 50 Index measures the total return of the 50 best performing stocks, based on the total reinvested return of each Constituent Stock since the previous rebalance date, of the 100 Constituents Stocks in the Cboe U.S. Large-Mid Cap 100 Index (CEQX). The Cboe U.S. Lag 50 Index measures the total return of the 50 worst performing stocks, based on the total reinvested return of each Constituent Stock since the previous rebalance date, of the 100 Constituents Stocks in the Cboe U.S. Large-Mid Cap 100 Index (CEQX).

Source: Cboe Global Markets

The VIX Index is based on real-time prices of options on the S&P 500 Index (SPX) and is designed to reflect investors' consensus view of future (30-day) expected stock market volatility. Cboe 1-Day Volatility Index® (VIX1D) estimates expected volatility by aggregating the weighted prices of P.M.-settled S&P 500 Index (SPX) puts and calls over a wide range of strike prices. The Cboe 3-Month Volatility IndexSM (VIX3M) is designed to be a constant measure of 3-month implied volatility of the S&P 500 (SPX) Index options.

Source: Cboe Global Markets

The Cboe S&P 500 Dispersion Index (DSPX) measures the expected dispersion in the S&P 500 Index over the next 30 calendar days, as calculated from the prices of S&P 500 Index options and the prices of single stock options of selected S&P 500 Index constituents, using a modified version of the VIX index methodology. The Cboe S&P 500 Implied Correlation Indices, including COR1M and COR6M, are the first widely disseminated market estimates of the average correlation of the stocks that comprise the S&P 500. The Cboe S&P 500 Implied Correlation Indices offers insight into the relative cost of SPX options compared to the price of options on individual stocks that comprise the S&P 500.

Source: Cboe Global Markets

The Cboe MSCI Emerging Markets BuyWrite IndexSM (BXEF) is a benchmark index designed to track the performance of a hypothetical buy-write strategy on the MXEF index. The Cboe S&P 500 BuyWrite IndexSM (BXM) is a benchmark index designed to track the performance of a hypothetical buy-write strategy on the S&P 500 Index. The Cboe S&P 500 Half BuyWrite IndexSM (BXMH) is a benchmark index designed to track the performance of a hypothetical covered call strategy. The BXMH Index is similar in design to the Cboe S&P 500 BuyWrite Index (BXM). However, the difference in methodology is as follows: the strategy only writes half a unit of an ATM monthly SPX call option while the long SPX Index position remains unchanged. The Cboe Validus S&P 500 Dynamic Call BuyWrite Index (CALD) tracks the value of a hypothetical rules-based investment strategy which consists of overlaying a basket of S&P 500 a.m.-settled standard expiry short call options over a long position invested in the S&P 500 with dividends reinvested (total return).

Source: Cboe Global Markets

The Cboe S&P 500 PutWrite IndexSM (PUT) tracks the value of a hypothetical portfolio of securities (PUT portfolio) that yields a buffered exposure to S&P 500 stock returns. The PUT portfolio is composed of one- and three-month Treasury bills and of a short position in at-the-money put options on the S&P 500 Index (SPX puts). The number of puts sold is selected to ensure that the value of the portfolio does not become negative when the portfolio is rebalanced. The Cboe Validus S&P 500 Dynamic PutWrite Index (PUTD) is designed to track the value of a rule-based investment strategy which consists of overlaying a basket of S&P 500 (SPX) a.m. settled standard-expiry short put options over a money market account invested at the 4-week daily Treasury Bill rate. The Cboe Russell 2000 PutWrite Index (PUTR) tracks the value of a hypothetical portfolio of securities (PUTR portfolio) that yields a buffered exposure to Russell 2000 Index stock returns. The PUTR portfolio is composed of an investment of $K in one-month Treasury bills and of a short position in an at-the-money puts on the Russell 2000 Index (RUT put), where K is the strike price of the put option.

Source: Cboe Global Markets

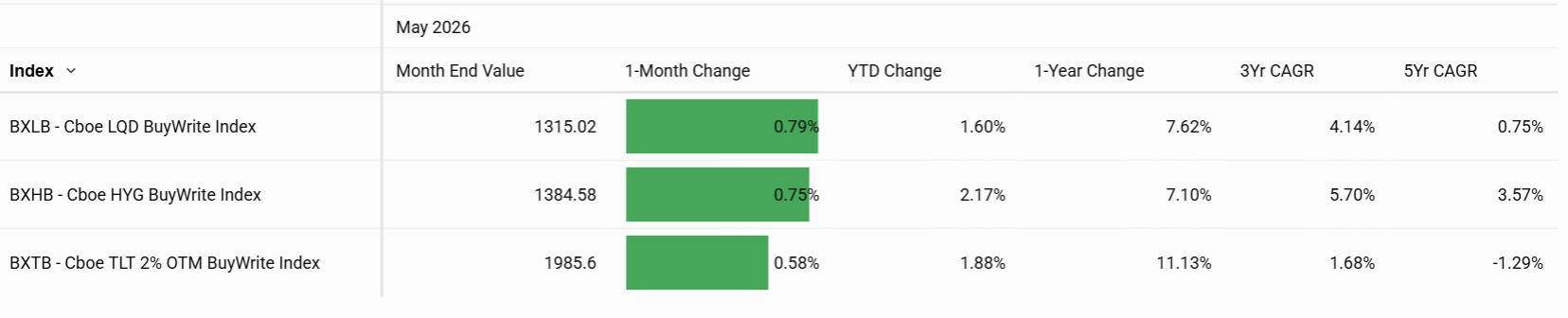

The Cboe HYG BuyWrite Index (BXHB) is designed to track the performance of a covered call strategy with a short iShares® iBoxx® $ High Yield Corporate Bond ETF (HYG) call option expiring monthly. The Cboe LQD BuyWrite Index (BXLB) is designed to track the performance of a covered call strategy with a short iShares® iBoxx® $ Investment Grade Corporate Bond ETF (LQD) Call option expiring monthly. The Cboe TLT 2% OTM BuyWrite Index (BXTB) is designed to track the performance of a covered call strategy with a short iShares® 20+ Year Treasury Bond ETF (TLT) Call option expiring monthly.

Source: Cboe Global Markets

The Cboe S&P 500 Enhanced Growth Index Series (SPEN) and Cboe S&P 500 Buffer Protect Index Balanced SeriesSM (SPRO) are part of a family of Target Outcome Indices. The Indices are designed to provide target outcome returns linked to the U.S. domestic stock market. The indices measure the performance of a portfolio of hypothetical exchange traded Flexible Exchange® Options (FLEX® Options) that are based on the S&P 500 Index.

Source: Cboe Global Markets

The Cboe VIX Tail Hedge Index (VXTH) tracks the performance of a hypothetical portfolio that -

The Cboe S&P 500 5% Put Protection Index (PPUT) tracks the performance of a hypothetical portfolio that -

Source: Cboe Global Markets

Cboe Bitcoin U.S. ETF Index (CBTX) options and Cboe Mini Bitcoin U.S. ETF Index (MBTX) options offer tools to hedge, capitalize on price movements, or express directional views on the world’s largest cryptocurrency without holding the asset.

The information herein is provided solely for informational purposes. Past performance of an index or financial product is not indicative of future results. Indices are not financial products that can be invested in directly, but they can be used as the basis for financial products (for example, without limitation, options, futures, mutual funds or exchange-traded funds) or to help manage portfolios. Nothing herein should be construed as investment advice.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/global-_disclaimers/. These products are complex and are suitable only for sophisticated market participants. In certain jurisdictions, Cboe Company products are only permitted for investment professionals, certified sophisticated investors, or high net worth corporations and associations. These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position. Market participants should put at risk only funds that they can afford to lose without affecting their lifestyle. © 2026 Cboe Exchange, Inc. All Rights Reserved.