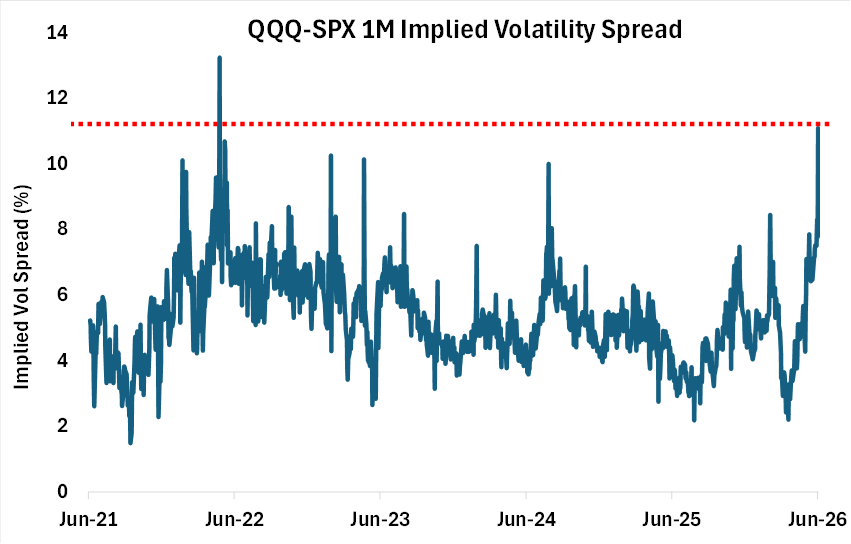

Implied volatilities jumped across asset classes last week as markets grappled with rising US-Iran tensions, higher bond yields, and a sharp pullback in Tech. Equity volatility led the increase, with the VIX® Index up over 6 pts wk/wk to 21.5%, rising from the 14th percentile low to the 86th percentile high. Within equities, Tech stocks led the spike in volatility, with the QQQ-SPX® 1M implied volatility spread widening to a 4-year high of 11% (see chart below). Both QQQ and SPX option volumes set new records on Friday, with SPX option volumes hitting a new high of 7.78M contracts (of which 64% was in 0DTE options).

Single stock volatility increased as well, though more marginally, with the VIXEQSM Index up just 0.3 pt as investors gravitated toward index hedges for protection. In other words, implied correlation jumped higher, with the COR1M Index more than doubling to 15% - albeit still trading at historically low levels. This suggests the sell-off, at least so far, remains mostly a positioning-driven unwind at the sector level, rather than a much broader macro sell-off. In fact, 6 of the 11 S&P sectors were up last week.

After weeks of chasing the right-tail, investor focus finally shifted last week to the left tail as hedging demand picked up notably. SPX 1M skew surged from a 1-year low to the 72nd percentile high. Retail sentiment also turned more bearish, with put buying making up 27% of all retail opening activity in the mega-cap Tech stocks on Friday (vs. just 15% a week ago).

Chart: QQQ-SPX Implied Volatility Spread Surges to 4-Year High